Amphenol ($APH) Deep Dive

Where data centers, space, robotics and electrification converge...

Hi, Investor! 👋🏼

I’m Jimmy, and welcome back to another edition of Jimmy’s Journal.

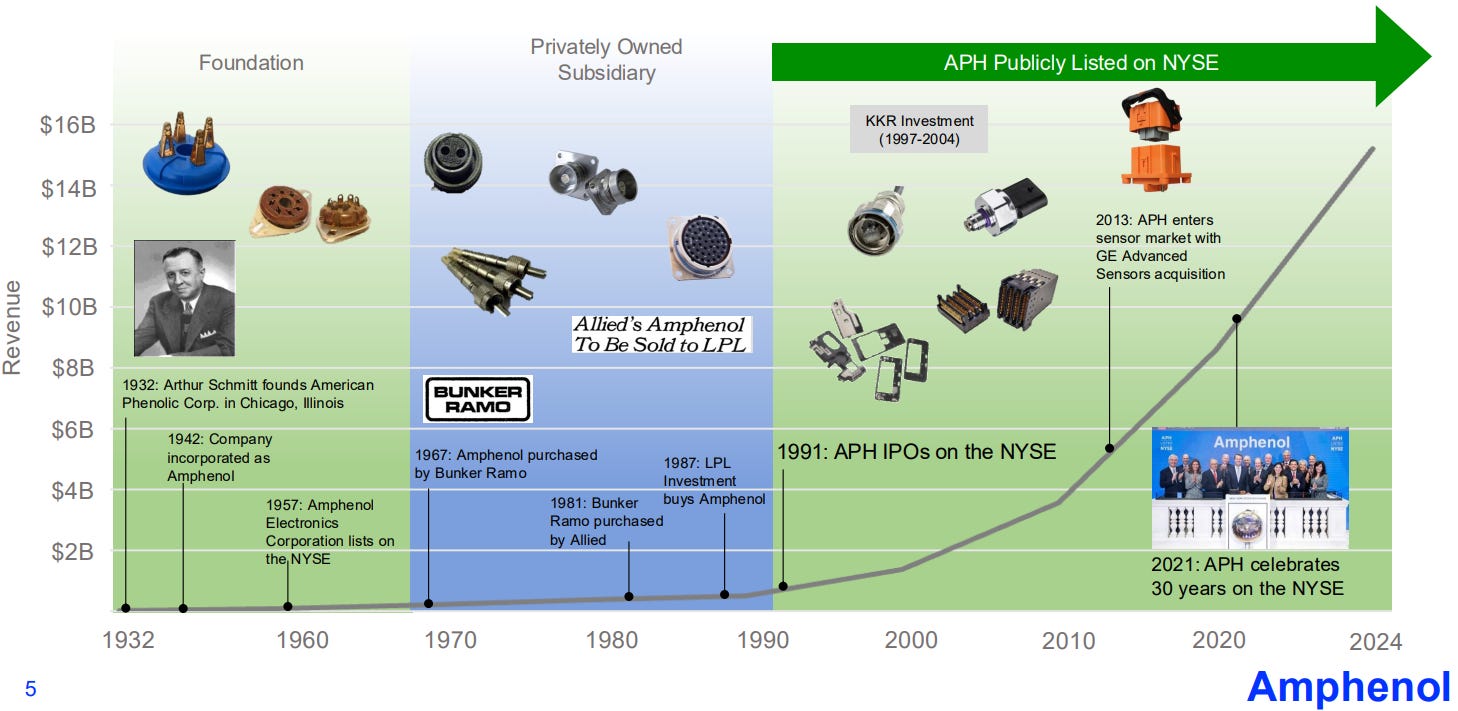

Amphenol’s origin story is so improbably long that it is almost easier to remember as a sequence of ownership changes than as a continuous narrative.

The company was founded in 1932 in Chicago by Arthur J. Schmitt as the American Phenolic Corporation, a small manufacturer of tube sockets for vacuum-tube radios.

The “Amphenol” name was a contraction that stuck.

World War II turned the company into a major supplier of military radio components - particularly the iconic AN connectors that became standard equipment across the U.S. military and remain, in updated form, a recognizable archetype of Amphenol’s product line nearly a century later.

The post-war decades were a slow march through American corporate ownership.

Don't get lost in the twists and turns:

The company listed on the NYSE in 1957 as Amphenol Electronics Corporation.

It was acquired by Bunker Ramo in 1967, which itself was absorbed into Allied Corporation in 1981.

In 1987, the LPL Investment Group took the company private.

In 1991, Amphenol returned to the NYSE as an independent public company.

Then, in a critical chapter for the modern Amphenol, KKR took a major stake from 1997 to 2004, restructuring the operating model and instilling the discipline that still pervades the company’s culture today.

The truly important figures in the modern story, however, are two men: Martin Loeffler and R. Adam Norwitt.

Loeffler joined Amphenol in 1974, became CEO in 1987 in the LPL era, took the company public in 1991, and served as CEO until 2009 before continuing as Chairman. He is the architect of what Amphenol calls “the Amphenolian culture” - a relentlessly decentralized, GM-led operating model that we will return to at length.

Loeffler retired from the Board at the May 2026 Annual Meeting, ending more than 50 years of affiliation with the company.

R. Adam Norwitt joined Amphenol in 1998 as General Counsel for Asia, became COO in 2007, succeeded Loeffler as CEO in 2009, and as of May 2026 also assumed the Chairman role.

Norwitt is, in my view, one of the more underrated industrial CEOs of his generation - a multilingual, hands-on operator who has spent his entire career inside the Amphenol system, speaks fluent Mandarin (he ran the Asia business directly for years), and has overseen a roughly seven-fold increase in revenue since taking the chief executive seat.

Under Norwitt, the company has executed more than 50 acquisitions in the last decade alone, expanded from roughly $3.5B in sales to over $23B, and transitioned from a primarily connector-focused business into a diversified interconnect, antenna, sensor, and assembly platform.

The compounding has been remarkable: from 2021 to 2025 alone, revenue more than doubled (+112%), adjusted EPS rose approximately +170%, and free cash flow expanded by $3.2b in annual run-rate.

What is striking about the trajectory is how little of it has come from heroic decisions. There is no single transformational deal that “made” Amphenol. There is no celebrated pivot, no signature product, no charismatic founder mythos.

The company has compounded for 35 years by doing the unglamorous work of selling roughly 250,000 SKUs to thousands of customers across seven end markets, acquiring smaller competitors at disciplined multiples, integrating them lightly, and trusting local general managers to outhustle the competition.

It is, in a real sense, the inverse of the modern tech narrative.

Simple, yet highly effective.

Our deep dive is organized into the following sections:

Company History (you just finished this one)

Industry Overview

Business Model

End Markets

Products and Value Proposition

The AI Goldrush and the Copper Question

Competitive Advantages

Competitive Landscape

The Acquisition Playbook

Culture and Governance

Financials and Long-Term Targets

Valuation

Main Risks

Investment Thesis

Final Thoughts

2. Industry Overview:

Market Size and Structure:

Amphenol estimates the global market for interconnect, value-add cable assembly, antenna, cable, and sensor-related products at approximately $500B in 2025.

To put that in context, this is meaningfully larger than the global semiconductor equipment market and roughly half the size of the global semiconductor market itself. It is, in absolute terms, one of the largest electronic component categories on earth.

Despite a generation of consolidation, the top ten players collectively account for well under 40% of the global market.

Amphenol - the second-largest player globally - holds well under 5% market share.

TE Connectivity, the leader by some measures, holds a similar share.

The rest of the market is split among dozens of regional, application-specific, and product-specific suppliers, many of them privately held or owned by larger industrial conglomerates.

The industry is fragmented because the demands placed on interconnect products are extraordinarily heterogeneous: a connector for a deep-sea oil platform shares almost nothing in common with a connector for a smartphone antenna, which shares almost nothing in common with a high-density backplane connector for an AI server.

The qualification cycles, the certification standards, the materials science, the manufacturing processes, and the customer relationships are entirely different across these applications.

Building a credible competitive position across the full range of applications takes decades of accumulated technology, customer relationships, and manufacturing know-how.

The corollary is that the industry naturally generates many specialists:

Glenair dominates a particular slice of mil-aero.

Rosenberger dominates a particular slice of RF coaxial.

JAE and Hirose dominate slices of Japanese consumer electronics.

Each has a defensible niche. Amphenol’s distinctive position is not that it dominates any single niche but that it credibly participates across virtually all of them.

Industry Economics:

The economics of the interconnect industry are characterized by four features that make it structurally attractive:

First, design-in revenue is sticky: most interconnect products are not commoditized off-the-shelf components but rather application-specific designs co-engineered with the customer’s product.

Once a connector or assembly is qualified into a customer’s design, it typically stays there for the product’s full life cycle - often a decade or longer in aerospace, defense, industrial, and automotive applications.

The switching cost for the customer is high: requalifying a new vendor means re-running expensive certification tests, modifying assembly processes, and accepting risk that the customer’s own product warranty is implicated.

Second, the industry has strong pricing power in the high-value-add segments: commoditized connectors in mobile devices and consumer electronics face brutal price pressure.

But high-speed signal interconnects, harsh-environment connectors, fiber optic systems, and complex backplane assemblies sell on the basis of performance and reliability, not price.

The engineering content embedded in these products supports gross margins that are structurally above the corporate average for most diversified industrials.

Third, the industry scales operating leverage well: interconnect manufacturing combines high-volume automation (for the commodity end of the line) with engineering-intensive design (for the value-add end).

The leading players can amortize R&D and global sales infrastructure over a broad product base, generating progressively higher incremental margins as revenue scales.

Amphenol’s incremental margins of 30-35% in recent quarters illustrate this dynamic.

Fourth, the industry is mildly cyclical but rarely deeply cyclical: demand is tied to the global capex and consumer electronics cycles, so revenue does fluctuate. But the diversity of end markets and the long-life nature of installed product mean that the industry does not experience the boom-bust dynamics common to semiconductors or capital equipment.

The 2020 pandemic produced a single quarter of mid-single-digit revenue decline at Amphenol, followed by an immediate recovery.

The 2008-2009 financial crisis produced a slightly deeper but still contained decline.

Secular Growth Drivers:

What is changing in the 2020s, and what makes the industry particularly attractive at this moment, is the convergence of several large secular forces that all drive interconnect content per electronic system higher.

Amphenol management organizes these around five themes, which I find genuinely useful as a framework:

Clean and Efficient: the electrification of everything - vehicles, heavy equipment, grid infrastructure, industrial power systems - dramatically increases the high-voltage, high-current interconnect content per system. An EV requires roughly 2-3x the dollar value of interconnect content of an internal combustion vehicle. A renewable energy installation requires substantial harsh-environment interconnect for high-voltage DC and AC systems.

Connected and Mobile: the continued proliferation of always-connected devices - from smartphones to industrial IoT sensors to autonomous vehicles - drives demand for antennas, RF interconnects, and low-power high-speed data interconnects. 5G and emerging 6G deployments add another layer of infrastructure spending.

High Speed: as data rates climb from PCIe Gen4 to Gen5 to Gen6 to Gen7, from 400G to 800G to 1.6T optical, from NVLink 4 to NVLink 5 and beyond, the engineering required to maintain signal integrity at these speeds becomes progressively more demanding. High-speed interconnect dollar content per system rises non-linearly with system complexity. This is the AI tailwind expressed in interconnect terms.

Increased Complexity: modern electronic systems integrate more components, more sensors, and more interconnect points than ever before. A modern car has nearly 100 interconnect points per system. A modern AI server has thousands. The proliferation of subsystems drives raw connector and cable assembly count higher independent of speed or power requirements.

Harsh Environment: as electronics penetrate increasingly demanding applications - under-hood automotive, space, defense, deep industrial, oilfield, subsea, medical implants - the ruggedized interconnect category grows. Harsh-environment products command premium prices and have substantially longer product lives than consumer-grade equivalents.

Stacking these drivers, the secular growth rate of the global interconnect industry sits in the mid-to-high single digits - a rate that Amphenol has consistently outgrown by 200-400 basis points per year through share gains.

The Consolidation Imperative:

A final point on industry dynamics worth flagging: the long-term trend is toward consolidation.

Customer concentration in many end markets (a handful of automotive OEMs, a handful of hyperscalers, a handful of defense primes, a handful of smartphone makers) increasingly demands suppliers with global manufacturing footprints, broad portfolios, and the financial strength to invest in next-generation technology.

The largest customers are actively consolidating their qualified vendor lists, and the players who lack scale find themselves squeezed out of meaningful design wins.

This dynamic disproportionately favors the largest, most diversified players - which means Amphenol and TE Connectivity at the global tier, with selected regional and product-category leaders surviving at the next tier.

For Amphenol specifically, this consolidation imperative is the structural driver that has powered its M&A program for thirty years and shows no sign of slowing.

The fragmented industry will not be fragmented forever, and Amphenol is one of the principal agents of its consolidation.

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

3. Business Model:

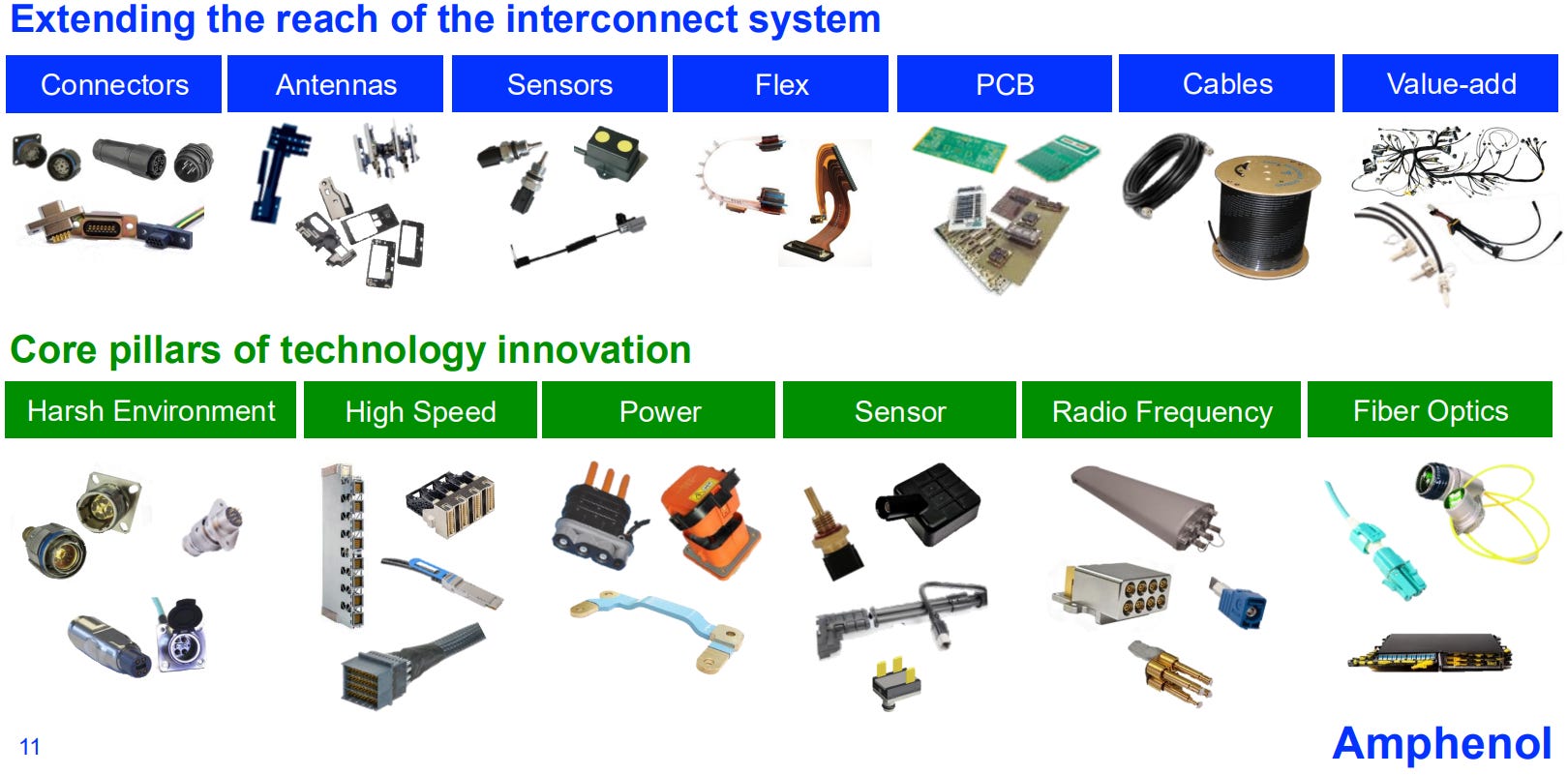

What does Amphenol actually sell?

When most investors think about technology, they think about the active components - the chips, the software, the algorithms.

Interconnects sit one layer beneath that abstraction. They are the physical infrastructure that moves electrons and photons between active components.

A connector is what plugs one circuit board into another.

A cable assembly is what carries signal from a transceiver to a switch.

An antenna is what converts radio frequency to electrical current.

A sensor is what converts physical state (pressure, temperature, position, vibration) into a signal a computer can read.

Individually, none of these components is glamorous.

A typical Amphenol connector might cost a few dollars. A high-end backplane assembly might cost a few hundred.

The unit economics are unspectacular. But two things make the aggregate business genuinely interesting:

First, interconnects are the unavoidable physical substrate of every electronic system. You can substitute one chip for another. You can rewrite the software. You cannot eliminate the need to move signals between components.

Every new generation of compute, communication, or sensing demands new generations of interconnects - typically with tighter tolerances, higher speeds, more channels, more power density, and more challenging environmental requirements.

The total addressable market expands mechanically with the volume and complexity of electronic systems.

Second, interconnects are designed in, not bought off the shelf. For any reasonably sophisticated system, the connector and cable design is part of the system engineering, locked in years before the product ships.

Once an Amphenol part is specified into a Boeing 787 airframe or an NVIDIA reference design, the switching cost for the customer is enormous - qualification testing, requalification of the system, supply chain changes, often re-tooling of automated assembly equipment.

This creates extraordinarily sticky revenue with long product lives. A typical defense or aerospace platform might generate revenue for 30 years after initial qualification.

Reportable Segments:

The company organizes itself into three reportable segments, all of which sell into all seven end markets:

Communications Solutions (52% of 2025 sales, $12.1B): is the largest and fastest-growing segment. This is where the high-speed, fiber optic, and radio frequency connectors live, along with the antennas.

It is the segment most directly exposed to the AI buildout, communications networks, and mobile devices.

The CCS (Connectivity and Cable Solutions) acquisition from CommScope, which closed in January 2026 for approximately $10.5 billion, slots into this segment and brings significant fiber optic capability for both IT Datacom and Communications Networks.

Harsh Environment Solutions (26% of 2025 sales, $5.9B): is the ruggedized portfolio - connectors, specialty cable, printed circuit boards, and assemblies that survive in environments where consumer-grade hardware would fail in minutes.

This segment is where defense, aerospace, and industrial harsh environment applications are concentrated.

Operating margins here are structurally above the corporate average because the qualification barriers are higher, the volumes are lower, and the price-per-unit captures the engineering content.

Interconnect and Sensor Systems (22% of 2025 sales, $5.2B): is the integration and sensor-heavy segment, encompassing value-add cable assemblies, busbars, power distribution systems, and the company’s sensor portfolio (force, gas, moisture, level, position, pressure, temperature, vibration).

This segment has the strongest exposure to electrification trends - both in vehicles and in industrial applications - and is also a focus area for the company’s expansion into adjacent technologies.

Operating Model:

What ties the three segments together - and this is critical to the investment thesis - is a shared operating model:

Each segment is led by a Division President reporting directly to the CEO. Underneath them are roughly 145 general managers running individual business units.

Each general manager has full P&L responsibility - they own the income statement and balance sheet of their business - and is compensated heavily on the results they deliver.

Corporate headquarters in Wallingford, Connecticut maintains perhaps a few hundred employees out of the roughly 170,000 in the company.

There is no centralized R&D function, no central sales force, no central manufacturing strategy. Each GM runs their factory, their engineering, their customer relationships, and their pricing.

This structure has profound implications for how Amphenol competes - and we will return to it when we discuss culture. For now, it is enough to note that the company has consciously chosen agility over scale economics, and has built a financial track record that suggests the choice was correct.

Already a Pro subscriber? Feel free to skip this section and jump straight to the full report below.

This article is exclusively available to paid subscribers of Jimmy’s Journal.

Inside the full report, we break down:

Why Amphenol’s connector portfolio is more strategically positioned for AI infrastructure build-out than the market’s valuation implies

How the company’s decentralized operating model creates durable competitive advantages that are structurally underappreciated

How valuation, target price, and competitive positioning evolve in the increasingly important debate between copper and photonics.

This is the type of institutional-quality research usually reserved for professional investors.

↳ Upgrade to Jimmys Journal Pro using the link below to unlock the full investment thesis: