Monthly Portfolio Update #4

February 2025: great start, terrible finish...

Hi, Investor 👋

I’m Jimmy, and welcome to the fourth edition of the Stellar Capital Management newsletter series! Through our fictional investment fund, I share high-conviction ideas to challenge conventional thinking.

In this edition, we’ll break down February 2025’s performance, key insights and trades from the month. Let’s dive in!

In case you missed it, here are some recent insights:

Subscribe now and never miss a single report:

Monthly Introduction:

February felt like two completely different months packed into one. The first half was incredible - by February 15th, our portfolio was up +7.59%, crushing the S&P 500’s +2.0% return. Meta ($META) was on an insane streak, logging 20+ consecutive green days. It almost felt too good to be true.

And, well… it was. The second half of the month brought a sharp correction, wiping out a big chunk of those early gains. We still closed February up +1.49%, while the S&P 500 finished down -1.42%, meaning we delivered +2.76 p.p. of alpha despite the pullback.

Zooming out, 2025 has been strong so far, with our portfolio up +12.61% YTD, outperforming the S&P 500 by +11.15 p.p.. Over the past 12 months, we’re sitting on a +35.39% return versus +16.05% for our main benchmark.

As usual, we always take a moment to reflect on the key theme of the month. In this edition, we’ll explore market volatility and the latest inflation data…

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

The Elephant in the Room:

February saw a downward revision in Q1 GDP growth, cut from 2.25% to 1.5% due to weak January consumption and a widening trade deficit. The Atlanta Fed’s GDPNow tracker fell to -1.5%, signaling downside risks. Despite this, the labor market remains strong, with 175k payrolls expected and unemployment holding at 4.0%.

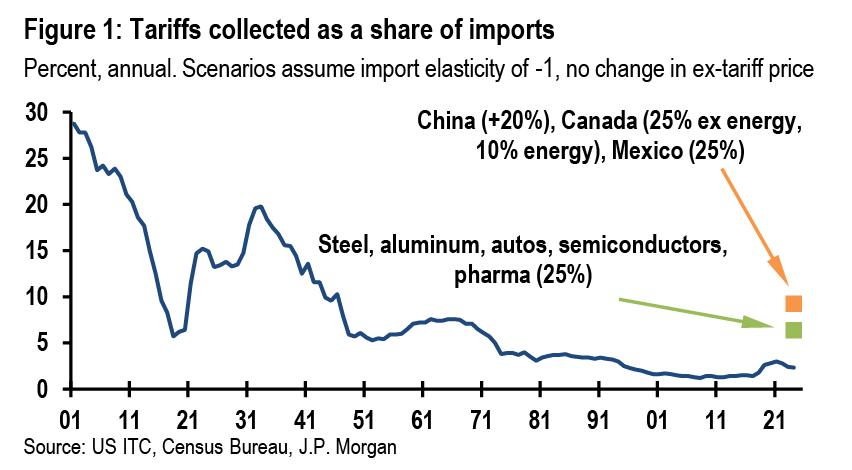

Trade policy uncertainty grew as new tariffs were announced. A 10% increase on Chinese imports is set to take effect, along with a possible 25% tariff on Canadian and Mexican goods. If fully implemented, these measures could slow economic activity and add inflationary pressure.

Inflation progress remained uneven. Core PCE inflation fell from 2.9% to 2.6% year-over-year but was slightly higher than expected. Consumer spending dropped 0.5% in January, its worst decline since 2021. A rebound in February is likely, but Q1 consumption growth is now projected at just 1.3% annualized.

The trade deficit widened by $31 billion, the biggest jump in decades. Imports surged 12%, driven by uncertainty and possible gold-related transactions. Some of this may be temporary, but tariffs could further disrupt trade flows.

Markets adjusted to these risks by pricing in three rate cuts for 2025, up from two last week. The February jobs report and Fed Chair Powell’s speech will be key in shaping expectations. ISM surveys will also reveal whether the services sector is stabilizing or weakening further.

With economic uncertainty rising, February was a reminder of how quickly conditions can shift. Inflation, trade, and growth remain key concerns heading into the rest of 2025.

Enjoying the content? Don’t miss out on more exclusive insights and analyses. Upgrade to paid now and stay updated.

Portfolio Overview:

As you already know, our portfolio is intentionally concentrated - reflecting our belief that generating alpha in a highly competitive market stems from focusing on a select group of high-conviction companies.

However, the correction in the second half of the month highlighted our concentrated exposure to a specific AI and tech growth thesis. We’ll be looking for more resilient opportunities throughout the month - and our paid subscribers will be the first to know which stocks we’ll be adding (or not) to the portfolio…

Additionally, we should see some changes in how the results are shared. I will soon release a spreadsheet with each trade in real-time, which will help with tracking.

Keep reading with a 7-day free trial

Subscribe to Jimmy's Journal to keep reading this post and get 7 days of free access to the full post archives.