Netflix ($NFLX) Deep Dive

Are you still watching?

Netflix ($NFLX) is one of those companies I had already been covering back when I worked as a buy-side equity analyst.

I never loved the company’s risk-adjusted return profile, and I used to think it was the least attractive FAANG (remember that acronym?) when weighing valuation against competitive advantages.

Over time, though, the company proved me wrong.

And the valuation, which once looked extremely stretched, is now sitting at much more attractive levels.

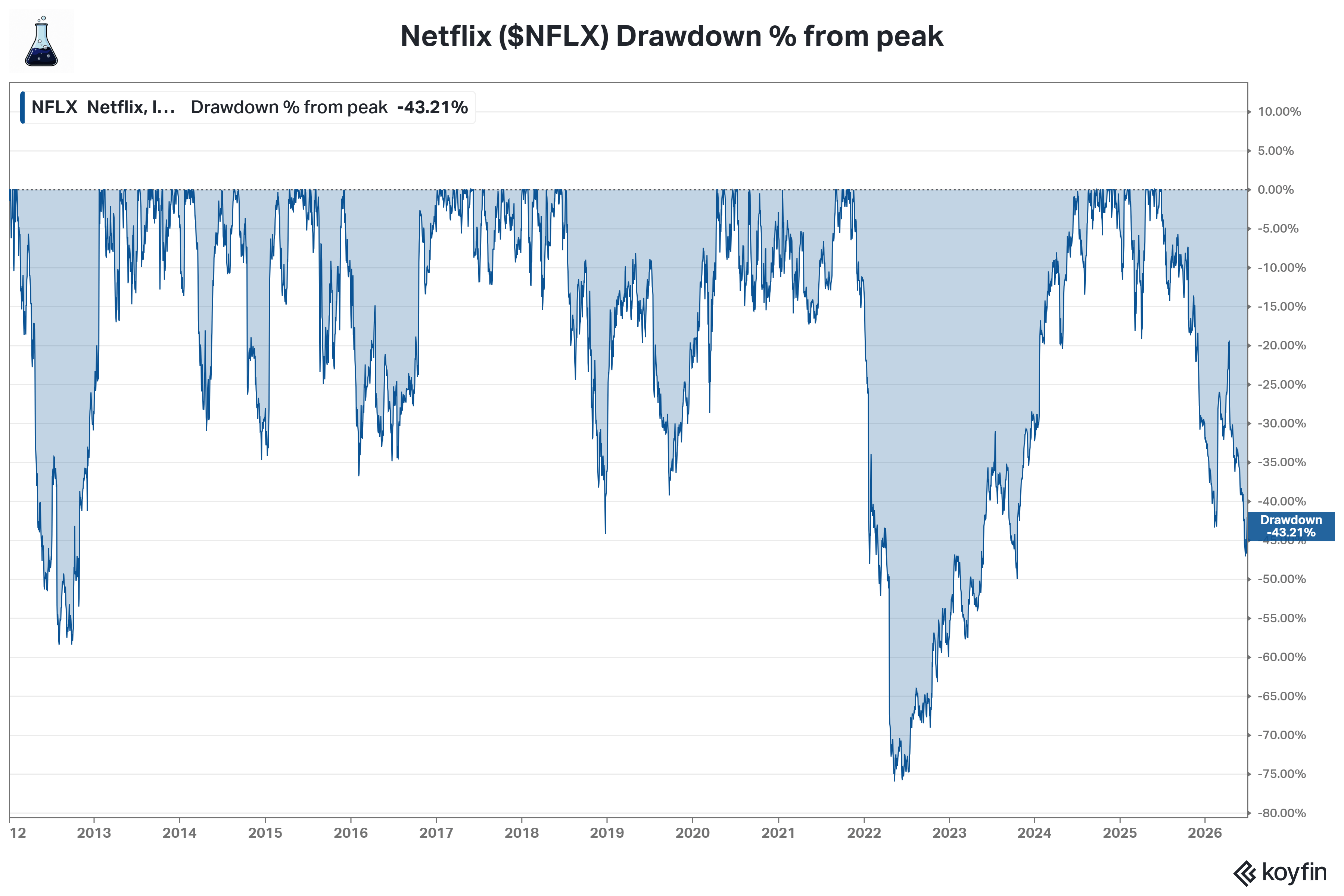

Netflix is currently going through an almost 45% drawdown, while its P/E multiple, which once stood around 100-130x, has compressed to less than 22x.

So… are we looking at a massive opportunity, or is Netflix a fading giant?

Everyone knows what Netflix does. The real goal of this deep dive is to unpack the company’s many moving parts in detail: screen time, competition, AI risks, culture, cohort monetization, future growth prospects, among others.

I hope you enjoy the read.

This deep dive is quite long and detailed, so we prepared a table of contents to help you navigate it.

Industry Overview

Company History

Business Model

Value Proposition

Netflix’s Flywheel

Netflix Originals and the Star-Making Machine

Durable Franchises and Screen Time

Live Sports

Gaming

Short-Form Videos: Netflix Clips

Advertising

AI: Risk or Opportunity?

Pricing Power and Churn

Culture: “No Rules Rules”

Competitive Advantages

M&As and Capital Allocation

Corporate Governance

Financials

Valuation

Investment Thesis

Main Risks

Are We Buying $NFLX?

1. Industry Overview:

Brief Context:

Over the last few years, the media and entertainment industry has undergone a structural shift that had been building for decades: the erosion of traditional television.

For a long time, TV was one of the most profitable business models in the world. It was this cash-generating machine that funded the growth of the major entertainment conglomerates, financed acquisitions, strengthened brands, and created some of the most valuable media assets in history.

In the beginning, the model was simple: major broadcasting networks like NBC and CBS distributed content for free and monetized their audiences through advertising. For consumers, access was limited to the signals their antennas could capture. But starting in the 1980s, the expansion of cable television - and later, satellite TV - completely changed that dynamic. Suddenly, consumers had access to dozens, and eventually hundreds, of channels in exchange for a monthly subscription.

That was the birth of the bundle: the pay-TV package that, in practice, every household was expected to buy. The economic logic was powerful. Since different people value different types of content, a broad package could serve a larger consumer base while increasing the monetization power of TV networks.

In 1980, only about 20% of American households had pay TV. By 2010, ~90% of US households were paying for some form of TV bundle.

From the 1990s onward, regulatory loosening accelerated industry consolidation and increased the bargaining power of the major TV networks over cable operators. The strongest channels became distribution anchors. ESPN, for example, helped Disney secure carriage for less in-demand channels. The same logic played out across the industry: highly desired networks carried a long tail of less popular assets alongside them.

Over time, this dynamic created a system that became increasingly favorable to TV networks - and increasingly expensive for consumers. The number of channels exploded, even though actual viewing behavior did not keep pace. Subscribers were paying for an ever-larger package while still watching only a small fraction of it.

The result was a steady transfer of value from consumers to the large media conglomerates. The average cable TV bill rose from $15/month in 1980 to close to $100/month in the decades that followed - growing far faster than inflation. In the late 1990s, the average subscriber paid for around 50 channels and watched just ~10. 15 years later, that same consumer was funding more than 200 channels while still consuming only a small portion of them.

This asymmetry was only possible because, for decades, TV networks controlled content distribution. Whoever controlled access to the consumer also controlled the economics of the industry.

But, as happened in so many other industries, the internet broke that logic. By dramatically lowering distribution barriers, it weakened one of traditional TV’s most important competitive advantages and opened the door to new models of consumption, monetization, and competition.

It was in this context that Netflix - no longer just a DVD-by-mail company, but the face of streaming itself - stopped being merely a convenient alternative and became a structural threat to the model that had sustained the entertainment industry for decades.

Not Netflix alone, but streaming as a broader category - including its competitors.

Streaming Wars: 1st Wave

After fiercely battling the traditional DVD rental model - most notably the now-bankrupt Blockbuster - Netflix eventually had to face a significant wave of new entrants in the very market it had helped create.

The Covid-19 pandemic marked a major turning point. Before then, traditional media conglomerates still had multiple ways to reach and monetize consumers through physical experiences, from movie theaters to theme parks. But once physical interaction became severely restricted, that advantage suddenly weakened.

In that environment, Disney - historically known for its theme parks and theatrical releases - watched Netflix add subscribers at an unprecedented pace and decided to move aggressively into streaming with Disney+. Warner followed with HBO, Apple with Apple TV, Paramount with Paramount+, and Amazon with Prime Video.

Suddenly, the market that many believed had high barriers to entry was flooded with competitors.

I decided to dig through some old emails I received back in 2021 and found the following chart from Chartr, which captures the market sentiment at the time quite well.

The headline of that same post read:

“Disney+ has hit 100 million paid subscribers, just 16 months since its launch.

That puts Disney roughly halfway to catching up to Netflix’s subscriber base, which is currently sitting at a lofty 204 million - but is growing much more slowly.

[…] Disney originally expected to have between 60 and 90 million subscribers by 2024. The company now expects something closer to 230 million subscribers by 2024.” — Chartr, 2021

To make matters worse, Netflix reported a loss of 200,000 subscribers in Q1 and guided for a loss of another 2M in the following quarter.

The result was an almost 70% collapse in the company’s market capitalization - which, in hindsight, proved to be one of the best entry points to invest in the business.

The market’s pessimistic projections never really materialized. Instead, Netflix emerged as the winner of the first wave of what we now call the Streaming Wars.

That’s because the strategic assumption behind the entrance of new players turned out to be wrong in a very specific way.

Legacy media companies believed their content libraries were the scarce and defensible asset. Owning Marvel, HBO, or a studio’s decades-old back catalog was supposed to be the moat. So they did what seemed logical at the time: pulled their content from Netflix, placed it inside their own walled-garden apps, and asked investors to reward subscriber growth instead of profitability.

For a while, the market played along.

Over the next 2-3 years, a full-scale content arms race followed. Industry-wide content budgets ballooned as every player tried to spend its way into relevance.

Then the bill came due…

Streaming, as it turned out, is a fixed-cost content business that only works at global scale. And almost every new entrant was domestic-first, subscale, or both. The economics were brutal. Disney’s direct-to-consumer (DTC) division lost more than $10B cumulatively before finally turning its first streaming profit in 2024. Peacock and Paramount+ burned cash for years.

The conversation, than, shifted from growth at any cost to profitability. Password-sharing crackdowns, ad-supported tiers, price increases, and, tellingly, re-licensing content back to competitors became the new playbook.

The barriers to entry everyone had dismissed turned out to be very real. They were just different from the old ones.

The moat was no longer spectrum, carriage deals, or a cable head-end. It was the ability to spend $18-20B a year on content and amortize that investment across more than 300M members in 190 countries. It was a global production engine, a recommendation and data system, and sheer consumer habit.

Netflix had assembled all four. Almost no one else could.

The chart, which seemed to point to an imminent Disney+ overtake, ultimately showed that Netflix’s moat was far stronger than the market had assumed.

![A Disney Começou a Deslizar nas Guerras de Streaming [OC] : r/dataisbeautiful](https://substackcdn.com/image/fetch/$s_!qLXO!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F88e951c8-3f82-4efa-a339-eccd2d85e0a0_1198x1198.png "A Disney Começou a Deslizar nas Guerras de Streaming [OC] : r/dataisbeautiful")

Streaming Wars: 2nd Wave

What could be better for a saturated market filled with unprofitable players than consolidation?

Consolidation is the word that defines the second wave of the Streaming Wars.

The logic becomes obvious once you understand what streaming really is: a fixed-cost content business that only generates attractive returns at global scale.

A prestige series costs roughly the same to produce whether 5M or 200M people watch it. The platform with the largest audience can spread that cost across the widest subscriber base, giving it structurally better unit economics every single time.

If you are small, you really have only two options: shut down or combine.

And combine is usually the preferred path.

That is why 2024 through 2026 became the years in which the streaming industry began consolidating at a pace and scale few had imagined.

Warner Bros Saga:

The clearest example is Warner Bros. Discovery, a company that was itself born out of one major merger and later became the target of another. WarnerMedia and Discovery combined in 2022, leaving the new company with a heavy debt load just as the streaming market was turning against the old “subscriber growth at any cost” playbook.

By 2026, WBD - owner of Warner Bros., HBO Max, and CNN - had become the prize in an open bidding war.

Netflix, breaking with its two-decade preference for building rather than buying, offered roughly $27.75/share in cash for the studio and HBO Max, deliberately leaving the declining cable networks behind. Paramount Skydance countered with a $31/share offer for the entire company, valuing WBD at roughly $77B in equity and well over $110B including debt. The bid was backed by Larry Ellison’s personal fortune, including a $45.7B equity commitment, alongside a debt package of approximately $57.5B.

Netflix, showing the capital discipline that has long separated it from the rest of the industry, chose not to raise its offer. It walked away and, in the process, collected a $2.8B break fee funded by Paramount. WBD shareholders approved the Paramount deal in April 2026, with the transaction still subject to a regulatory review expected to last 12 to 18 months.

Paramount+:

Paramount’s own story reflects the same pattern one layer down.

The company acquiring WBD is itself a recent product of consolidation. Paramount and Skydance completed their own merger in 2024, again with Ellison capital behind it. In just two years, Paramount went from being a struggling, subscale player widely seen as potential prey to becoming the predator absorbing one of the largest content libraries in the industry.

That’s consolidation feeding on consolidation. The survivors are getting bigger by swallowing one another.

Fox and Roku:

Rather than buying more content, Fox bought distribution. In June 2026, Fox agreed to acquire Roku for almost $22B, combining its live news and sports assets, along with Tubi, with Roku’s operating system, advertising platform, and direct relationship with more than 100M streaming households.

Fox had been the last major broadcaster without a scaled streaming anchor. With Tubi and The Roku Channel, it instantly gained two of the largest free, ad-supported streaming services in the country, along with a real foothold in connected-TV advertising - the fastest-growing pool of ad dollars migrating away from linear television.

The deal would make the combined company one of the three largest players in US television by share of viewing.

Comcast:

Comcast is also dismantling and rearranging itself in real time. The company is spinning off NBCUniversal’s declining cable networks into a separate entity, Versant, preparing to split into two independent businesses, and positioning NBCUniversal for whatever strategic optionality the next round of dealmaking might bring. Many observers expect NBCUniversal to attract potential acquirers once it stands on its own.

Even Comcast’s European arm has joined the consolidation wave, with Sky agreeing to acquire ITV’s media and entertainment business for around $2.14B.

Disney+:

Disney, meanwhile, took a different step. After years of running Hulu as a partially owned asset, the company bought out Comcast’s remaining stake, brought Hulu fully inside its ecosystem, and now sells Disney+, Hulu, and ESPN as a single bundle.

The irony of it all is fascinating…

The internet broke the cable bundle by collapsing the cost of distribution and fragmenting a tidy oligopoly into a chaotic field of competing apps. Barely a decade later, that same field is collapsing back in on itself through mega-mergers, re-bundling, and a handful of scaled conglomerates absorbing the rest.

The industry that spent the 2010s unbundling is now spending the 2020s re-bundling.

And sitting above all of it, curiously untouched by the merger frenzy, is the company that started the fire.

Netflix doesn’t need to consolidate.

It already has the scale everyone else is scrambling to assemble: more than 325M members, a presence in 190 countries, a $20B content budget, and the free cash flow to fund it through almost any downturn.

Found this content valuable? Leave a restack and like this article. These small actions go a long way in helping more people discover our work.

2. Company History:

Reed Hastings and Marc Randolph founded Netflix in 1997 as a DVD-by-mail service. Two years later, in 1999, the company introduced the subscription model that would become its defining feature.

The journey was not always smooth…

With a complex and still unprofitable business model, Netflix was offered to Blockbuster in the early 2000s for $50M. Blockbuster turned it down.

The first major inflection point came in 2007, when Netflix launched streaming and, crucially, treated it as an opportunity to cannibalize itself rather than as a threat to its profitable DVD business.

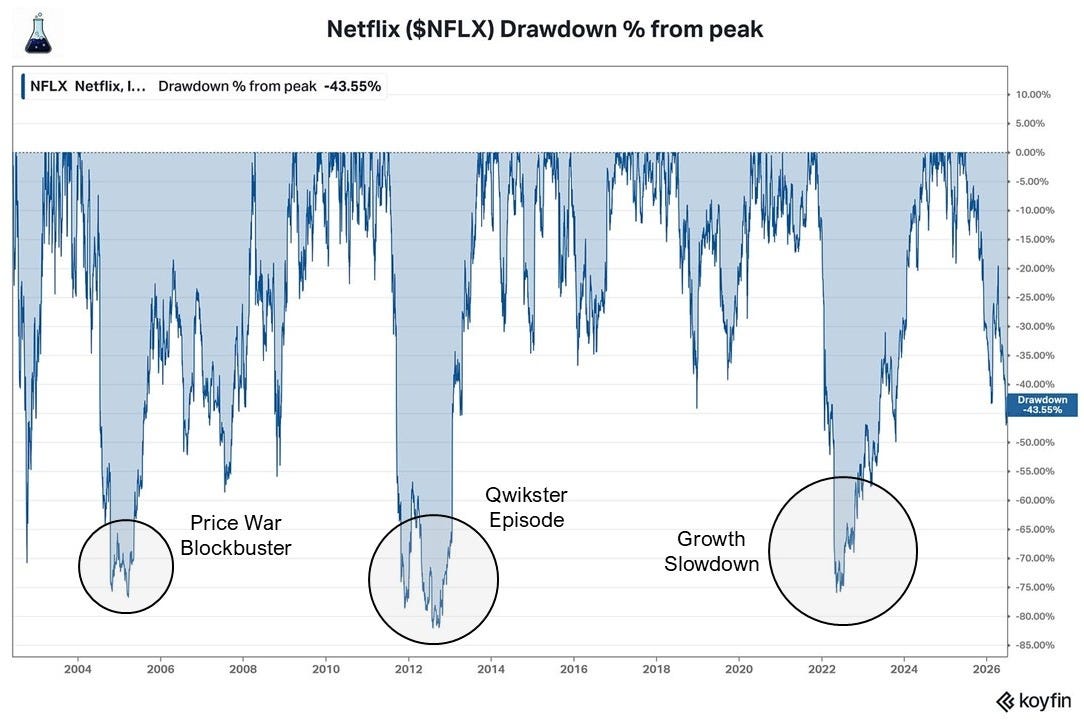

The second, and perhaps more instructive, moment came in 2011 with the Qwikster episode. Hastings attempted to separate streaming and DVDs into two different services, effectively raising prices in the process. The backlash was immediate, since Netflix lost 800,000+ subscribers in a single quarter - and the stock collapsed.

At that point, the market concluded that Netflix was little more than a commoditized content renter with no real pricing power.

It was wrong… but it would take years for that to become obvious.

The third act was the one that shaped the modern Netflix. In 2013, the company released House of Cards and Orange Is the New Black, proving that it could create its own hits rather than simply rent other people’s content. Then, in January 2016, Netflix turned on the service in approximately 130 countries almost overnight.

Hastings has repeatedly described that global launch as his favorite memory at the company. After all, that decision separated Netflix from almost every domestic-first competitor that would later try to follow it.

Netflix’s fourth act is still very recent, and its consequences are still unfolding.

After the growth slowdown of 2022, when the market briefly concluded that the story was over, management responded with two moves that many observers disliked at the time:

cracking down on password sharing and

launching a cheaper, advertising-supported tier.

Both were treated as signs of desperation.

Both helped reaccelerate the business.

By the time we reach the period covered in this deep dive, Netflix has surpassed 325M paid memberships and stopped reporting quarterly subscriber counts altogether, deliberately shifting the conversation away from pure subscriber growth and toward revenue, margins, engagement, and long-term monetization.

3. Business Model:

Netflix’s business model is remarkably easy to understand, especially because the service is part of everyday life for hundreds of millions of people around the world.

By LogoFeverYT On")

Revenue Drivers:

At its core, revenue is generated from the monthly fees paid by subscribers across a range of plans, plus the newer and increasingly important advertising revenue stream.

In the United States, Netflix recently repriced its plans to $8.99/mo for the ad-supported tier, $19.99/mo for the standard plan, and $26.99/mo for the premium plan, after pushing through another round of price increases in early 2026. The ad-supported plan is deliberately the cheapest entry point into the service, and it now represents well over 60% of new sign-ups in countries where the advertising tier is available.

The company’s most important growth driver is average revenue per membership, or ARPU. Management can expand ARPU through three main levers:

Raising prices;

Moving members into higher-priced tiers; and

Layering advertising revenue on top of the ad-supported plan.

This is also why Netflix stopped guiding investors toward net subscriber additions the way it used to. Management wants the market to focus less on short-term membership growth and more on lifetime value.

In my view, that shift was brilliant.

Subscriber growth is a short-term metric that can easily understate the long-term value creation of the business. It says little about Netflix’s ability to monetize the same user more effectively over time, especially as advertising becomes a larger part of the model.

Revenue by Geography:

Based on Q1 2026 results, Netflix’s geographic mix is still heavily weighted toward mature markets, but the growth is increasingly coming from emerging ones.

UCAN, which includes the United States and Canada, generated $5.25B in revenue in Q1 2026, representing about 43% of total revenue. It remains Netflix’s largest and most profitable region, but growth was also the slowest among the four geographies, at +14% y/y, reflecting a market that is already deeply penetrated.

EMEA, which includes Europe, the Middle East, and Africa, generated $4.0B, or about 33% of total revenue. Reported growth was +17% y/y, although only +12% on a FX-neutral basis.

LATAM generated $1.5B, representing about 12% of revenue, with growth of +19% y/y (+18% FX-neutral).

APAC also generated nearly $1.5B (12% of revenue), and was the fastest-growing region, with revenue up +20% y/y (+19% FX-neutral).

UCAN and EMEA generate almost 3/4 of revenue, while LATAM and APAC, despite representing only ~24% combined, are growing 40-45% faster than UCAN.

On the last figures Netflix disclosed by region (FY2024, before it stopped reporting ARPU and memberships regionally), monthly ARPU was about $17.20 in UCAN, $10.96 in EMEA, $8.01 in LATAM, and $7.31 in APAC, against a global average near $11.70.

In other words, UCAN’s ARPU is more than 2.3x higher than APAC’s, which explains why the region is now largely a price-and-advertising story. Subscriber penetration is already high, and volume growth is naturally limited.

APAC and LATAM, meanwhile, are still volume-and-mix stories, with substantial room for ARPU to rise as middle-class incomes grow, smartphone penetration increases, local-content investment deepens, and the payable user base expands.

Cost Drivers:

If Netflix increasingly behaves like a kind of marketplace for movies and TV shows, why isn’t it valued like a software company? And why is its gross margin still only around 50%?

Both questions lead us to the most important line in Netflix’s income statement: cost of revenues, or COGS in traditional financial statement language.

Netflix’s own Form 10-K explains why:

“We recognize content assets (licensed and produced) as ‘Content assets, net’ on the Consolidated Balance Sheets. For licensed content, we capitalize the fee per title and record a corresponding liability at the gross amount of the liability when the license period begins, the cost of the title is known and the title is accepted and available for streaming. For produced content, we capitalize costs associated with the production, including development costs, direct costs and production overhead, as costs are incurred.

Based on factors including historical and estimated viewing patterns, we amortize the content assets (licensed and produced) in ‘Cost of revenues’ on the Consolidated Statements of Operations over the shorter of each title’s contractual window of availability, estimated period of use or ten years, beginning with the month of first availability. The amortization is on an accelerated basis, as we typically expect more upfront viewing, and film amortization is more accelerated than TV series amortization. On average, over 90% of a licensed or produced content asset is expected to be amortized within four years after its month of first availability. We review factors that impact the amortization of the content assets on a regular basis. Our estimates related to these factors require considerable management judgment.” — Netflix, Form 10-K, 2026

If that was difficult to understand, here is a simpler explanation, written by myself:

The content produced by Netflix is capitalized as an asset - meaning capex - and amortized over time as it is watched - meaning a cost.

Most companies report depreciation (D&A) as an expense, because it is usually related to software licenses, machinery, and equipment. However, because Netflix is the largest buyer of content on the planet, and the production of movies and TV shows is an essential factor for its subscription revenue to exist, they place it as a cost - right below net revenue.

The assumption is that this content will be watched - and therefore amortized - over a 10 year period, losing 90% of its value within 4-5 years.

Although this makes sense, the logic is also quite debatable, especially because it is highly intangible and because there is uncertainty around the “durability” of franchises. Ernst & Young, the auditor of the company’s financial statements, even adds an asterisk to this point. Nothing that breaks the thesis, but certainly something worth monitoring.

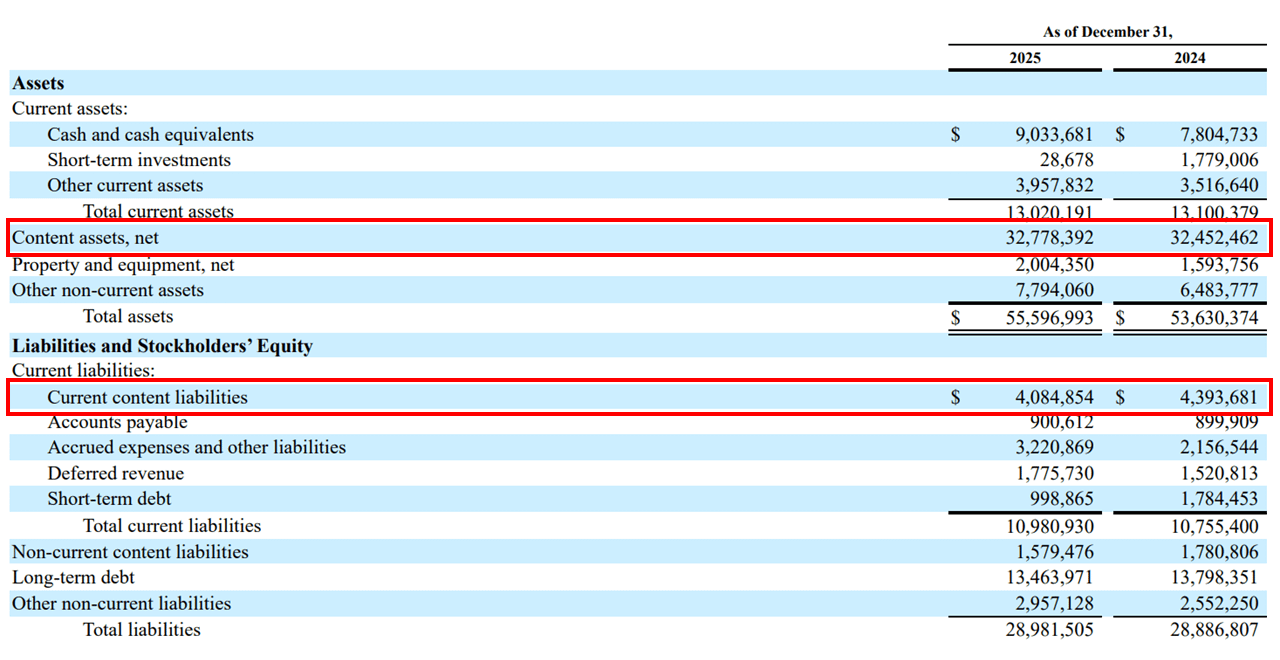

In total, the company carries $32B of content assets on its balance sheet, with Netflix Originals, or produced content, representing ~63% of total content assets and ~46% of Q1 2026 amortization.

Another very important item, although disclosed only in the footnotes, is content obligations. The company has “off-balance-sheet” liabilities that have not yet been recognized, related to contractual obligations for the development of new content.

In the company’s own disclosure:

“As of December 31, 2025, content obligations were comprised of $4.1 billion included in ‘Current content liabilities’ and $1.6 billion of ‘Non-current content liabilities’ on the Consolidated Balance Sheets and $18.4 billion of obligations that are not reflected on the Consolidated Balance Sheets as they did not then meet the criteria for recognition.”

When the company says “did not then meet the criteria for recognition”, it is basically saying that the title is not yet available in the catalog. Once it becomes available, it will be recognized on the consolidated balance sheet, together with its corresponding offset in “Content assets” on the asset side.

I would usually leave these observations for the balance sheet section, but given how important they are to the investment case, I decided to touch on them here in the business model section to make sure everyone has access to the context.

Netflix spent $18B on content in 2025 and is guiding to about $20B in 2026, a +10% increase y/y.

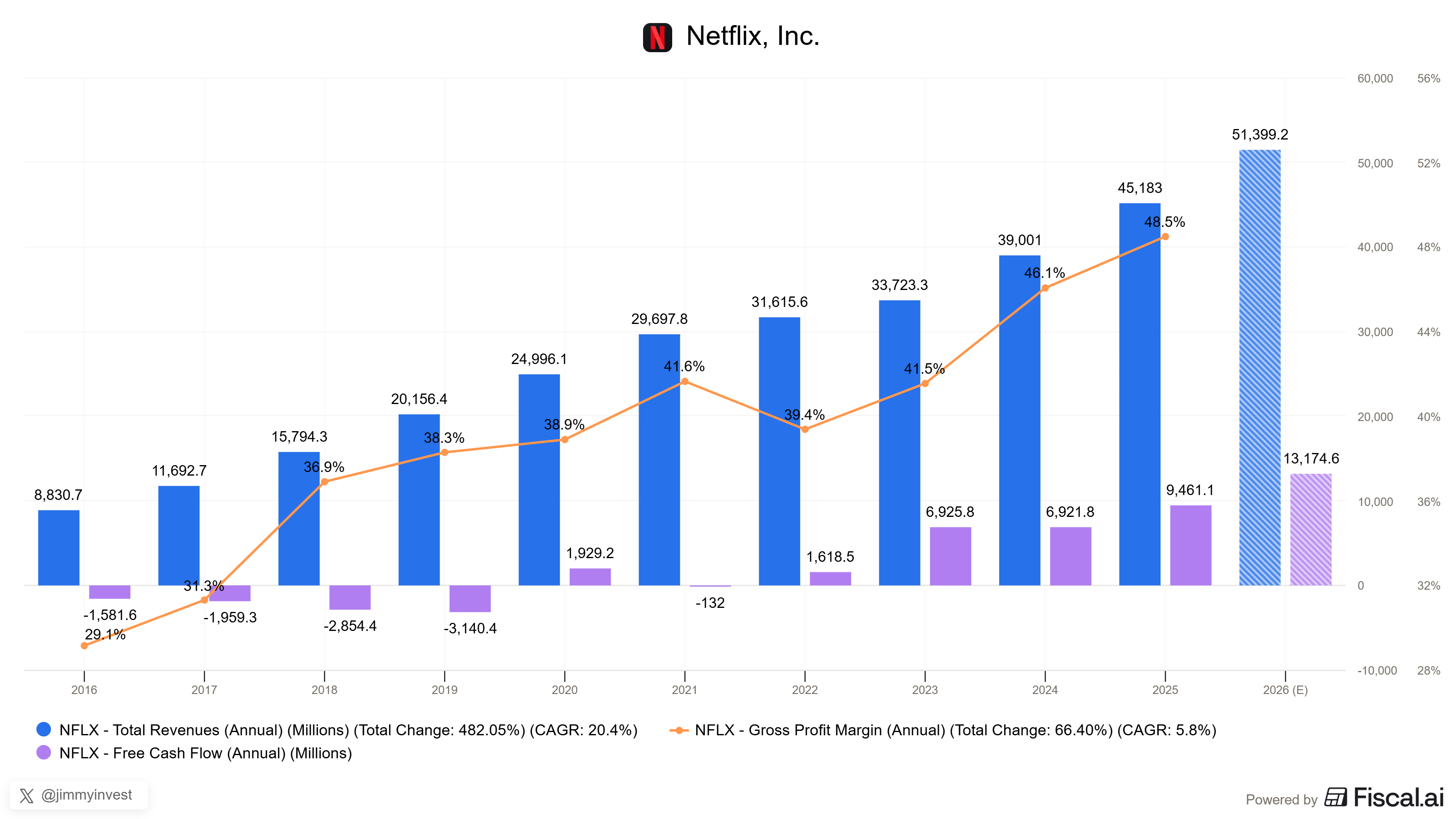

The company’s margin expansion over the last few years has come almost entirely from this line. In 2016, content spending represented around 78% of revenue. By 2024, that ratio had fallen to ~41%, and based on 2026 guidance, it should land near 39%.

Netflix targets a cash-content-to-amortization ratio of 1.1x, which tells us that the company is still spending cash slightly ahead of what it is expensing. In other words, this remains a growing content library rather than a business being run in harvest mode.

The operating margin, of course, has followed the same trajectory, with management guiding to 31.5% in 2026 (vs. 29.5% in 2025).

While bears describe this as an accounting maneuver, bulls see it as the mechanical result of a global fixed-cost content base being spread over an ever-larger revenue line.

Enjoying the content? Upgrade to Jimmy’s Journal Pro to unlock the full experience - now with 25% OFF before prices increase in the next few days.

4. Value Proposition:

For an audience that grew up watching pay TV, Netflix’s value proposition is almost incomparable.

In the United States, the average TV subscriber watches approximately 4h of content per day and pays around $120/month to the cable operator. That implies a cost of approximately $1.00/hour watched.

By contrast, the average Netflix user watches around 2h of content per day and pays $19.99/month for the service, which translates into a cost of about $0.31/hour watched.

In other words, Netflix offers a better product while charging 65-70% less per hour of consumption.

There is also another important piece of the value proposition: time.

Whether in the United States, Europe, or Japan, each hour of traditional TV typically includes 12 to 20 minutes of advertising. Without commercials, 2 hours of Netflix save the user between 24-40 minutes of ads per day.

Over the course of a year, that means the average Netflix user avoids approximately 200h of commercials - the equivalent of more than 8 full days.

The interesting part is that, over time, this value proposition has continued to evolve:

The ad-supported plan introduced a more affordable tier, allowing Netflix to absorb a segment of consumers who previously may not have been willing or able to subscribe.

Gaming extended the power of its franchises beyond passive viewing.

And live sports helped Netflix reach a portion of the audience that historically had not been a natural fit for the company.

When compared with its traditional media competitors, Netflix also enjoys a much cleaner strategic position.

An incumbent like Disney or Comcast, for example, has to manage a delicate transition into the DTC world while simultaneously dealing with the secular decline of other business lines - a decline that is often accelerated by any eventual success in streaming.

That creates a difficult incentive structure.

Netflix sits on the opposite side of that spectrum, both organizationally and strategically, and also in the mind of the consumer.

According to marketing consultancy Siegel+Gale, creator of the Global Brand Simplicity Index, Netflix has been ranked as one of the simplest brands in the world.

The brand became the product.

5. Netflix’s Flywheel:

I have always been particularly drawn to platform businesses because they changed the rules of traditional economics, growing through a self-reinforcing virtuous cycle: the flywheel.

And Netflix’s flywheel is one of the clearest and most powerful examples.

More members generate more revenue. More revenue funds more content. Better and broader content drives higher engagement and retention, while also fueling fandom and word of mouth, which in turn attracts even more members.

Underneath this entire loop sits a data layer:

More viewing generates more behavioral data.

More data improves recommendations.

Better recommendations increase engagement.

And, critically, that same data also helps Netflix decide which content to produce, license, or buy next.

And in the age of “vibe coding,” it is easy to underestimate Netflix’s technological relevance, especially when user interfaces can seemingly be replicated with a single prompt.

That conclusion, however, misses the value of the technological arsenal Netflix has built over the years to deliver the best possible user experience.

This includes:

A/B testing systems that dynamically change each title’s cover art to maximize conversion;

Proprietary video compression algorithms, such as Dynamic Optimizer, which not only adjusts streaming quality to connection speed but also modulates compression scene by scene to minimize buffering;

Proprietary recommendation algorithms, which divide the library into 80,000+ of subcategories and use AI to personalize recommendations for each profile;

A long list of features carefully designed to remove friction from the user experience, from remembering where a user stopped watching, to skipping intros and credits, autoplaying the next episode, and adapting trailers for mobile users; and

New consumption formats, such as interactive content that allows viewers to influence the direction of a story, as well as games that deepen the integration between mobile devices and the TV experience.

The interface may look simple, but the technology underneath it is anything but.

Found this content valuable? Leave a restack and like this article. These small actions go a long way in helping more people discover our work.

6. Netflix Originals and the Star-Making Machine:

The logic behind Netflix Originals, launched in 2013, is what allowed Netflix to survive as a true IP owner once competitors began pulling their titles from the platform to build their own streaming services in 2021-2022.

But beyond being a survival mechanism, the “own instead of rent” strategy is also an improvement mechanism.

As we discussed earlier, Netflix Originals represent 63% of the company’s total invested content capital - and that share should continue to rise over time.

Combine a massive content investment budget with a gigantic subscriber base, and Netflix gets two powerful levers: (i) creating the next generation of stars, and (ii) resurrecting forgotten or under-monetized titles.

The first lever is talent creation.

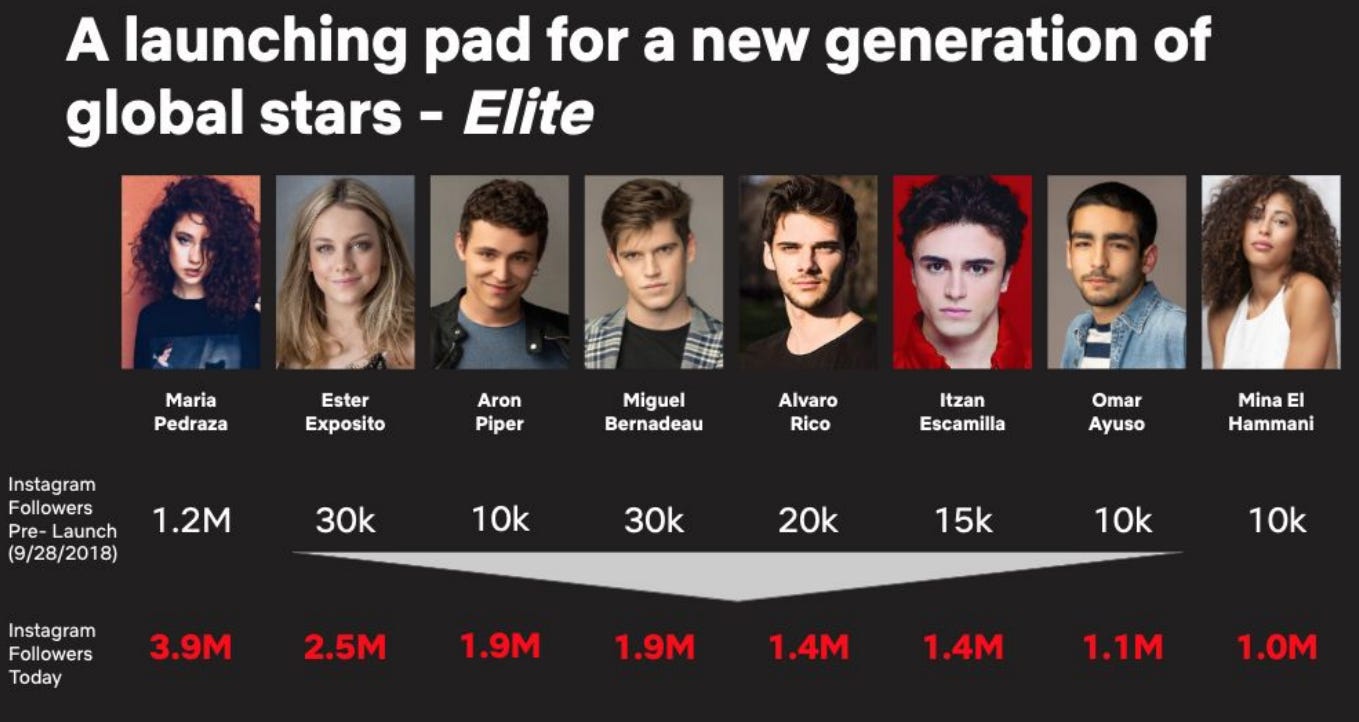

Take Elite, an example Netflix itself has used. Before the show launched, most of its lead actors were largely unknown. After being exposed to Netflix’s enormous global subscriber base, they became recognizable stars, saw their market value rise materially, and grew their social followings exponentially.

That makes Netflix highly attractive for emerging actors.

More importantly, Netflix owns the IP behind these projects, and that IP can extend far beyond the original series into spin-offs, films, games, live experiences, merchandise, and, increasingly, the vertical-video and social layer. In other words, a higher lifetime value per successful franchise.

And Elite is far from the only example. Millie Bobby Brown through Stranger Things, Jenna Ortega through Wednesday, and Lee Jung-jae through Squid Game all show how Netflix can transform actors into global names. Lee Jung-jae, in fact, went on to win an Emmy shortly after Squid Game became a worldwide phenomenon.

The second lever is also very important: Netflix can resurrect third-party content that failed, stalled, or underperformed elsewhere.

The company can license titles from other studios at relatively low cost, place them in its catalog, push them through its recommendation engine, and extract far more value from them than their original owners were able to capture.

A symbolic case is the psychological thriller You. The series was originally produced for Lifetime, where it never cleared a daily average of 700,000 viewers and was effectively cancelled after its 1st season. Netflix acquired it, put it in front of its global base, and let the recommendation engine do the routing. Within four weeks, more than 40M accounts had watched it.

Suits, legal drama ended in 2019, had been available on Peacock and Amazon for years with modest results. After landing on Netflix in mid-2023, it accumulated 57.7B viewing minutes over the year, topped Nielsen’s overall streaming chart for a record 12 consecutive weeks, broke the record for the most-watched acquired title with 3.7B minutes in a single week, and finished as the most-streamed show in the United States that year, edging out The Office.

Cobra Kai, which started on YouTube Red before becoming a Netflix hit, and Manifest, cancelled by NBC and later revived by Netflix after topping its charts, follow the same logic.

The “Netflix effect” is a repeatable mechanism through which Netflix can buy underperforming catalog content at a discount to originals and convert it into top-of-chart engagement.

That happens because Netflix’s distribution and recommendation layer is often worth more than the content it wraps.

This lowers the effective cost of filling the catalog and helps explain why content spending can keep falling as a share of revenue even as engagement remains strong.

7. Durable Franchises and Screen Time:

Owned franchises are what truly anchor Netflix’s screen-time leadership, and the concentration is meaningful.

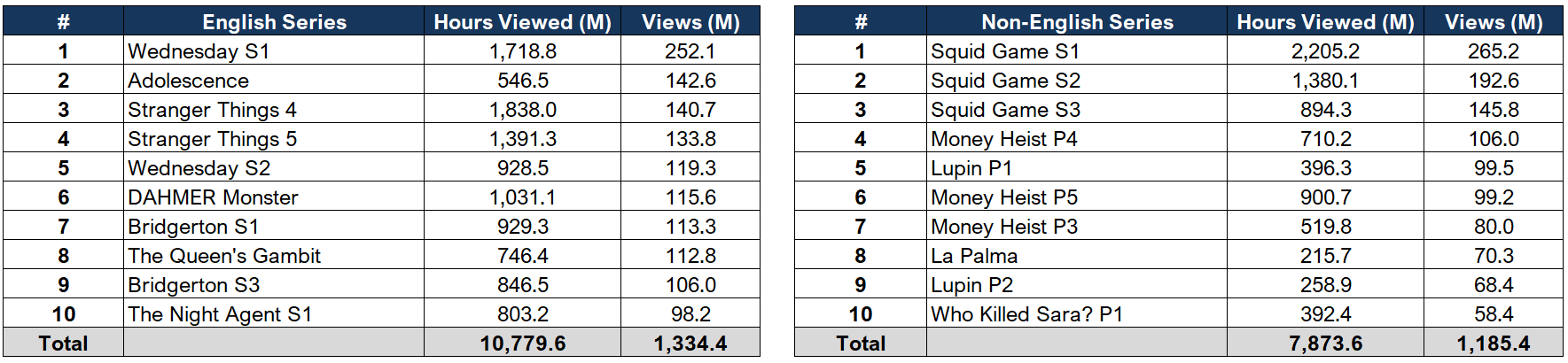

On Netflix’s all-time viewership rankings, Squid Game Season 1 has generated 265M views and about 2.2B hours watched. Wednesday Season 1 sits around 252M views. Stranger Things Season 4 delivered 141M views and about 1.8B hours watched, while both its final season and Wednesday’s second season landed near the top of the platform’s rankings.

On the film side, KPop Demon Hunters became Netflix’s most-watched title ever, with 325M views.

On Nielsen’s US panel, Stranger Things alone generated more than 15B viewing minutes in a single month around its final season, ranking as the most-watched streaming title in the country for consecutive months.

These franchises matter disproportionately…

A small number of owned tentpoles drive an outsized share of engagement, acquisition, and fandom - the kind of fandom that later extends into games, merchandise, live experiences, social media, and future spin-offs.

This is the “flywheel inside the flywheel”.

The biggest IP gets watched, re-watched, discussed, memed, extended, and monetized across multiple surfaces. That is exactly the type of durable, compounding value Netflix’s content budget is supposed to create.

Which is why the emerging data on returning seasons also deserves attention…

In mid-2026, Bloomberg reported that several of Netflix’s largest returning series were losing more than 50-60% of their audience between seasons within the first 4 weeks of release:

Avatar: The Last Airbender reportedly shed around 60% of its week-one views in Season 2;

One Piece dropped more than 30%;

Beef fell around 70%;

An earlier example, The Recruit, went from 24M views to less than 14M, a decline of more than 40%.

The comparison with the rest of the industry is what makes this especially interesting. Broadcast series - and notably Apple TV shows - have generally seen viewership build across seasons, while many Netflix shows tend to peak on debut and fade afterward.

Management, including both co-CEOs, has publicly downplayed the concern, even as the company studies its own data to understand why this pattern is emerging.

In the first 6 months of 2026, Netflix had only 2 truly large hits.

Enjoying the content? Upgrade to Jimmy’s Journal Pro to unlock the full experience - now with 25% OFF before prices increase in the next few days.

8. Live Sports: The Golden Age

Netflix spent years insisting it had no interest in live sports. Since then, it has built one of the more disciplined sports strategies in media - and the logic is visible in the numbers.

The anchor deal is WWE: a 10-year agreement worth $5B, or about $500M/year, under which Monday Night Raw moved exclusively to Netflix worldwide starting in January 2025. The agreement also includes international rights to WWE’s other weekly programs, pay-per-views, and library.

On the NFL side, Netflix acquired a package of Christmas Day games - two in 2024, each drawing about 24M viewers and ranking as the most-watched English-language programming on the platform that week - with the package scaling to five NFL games in the 2026 season, plus NFL Honors during Super Bowl week.

Netflix also holds US rights to the 2027 and 2031 FIFA Women’s World Cups, the 2026 World Baseball Classic - whose broadcast in Japan drew 31.4M viewers and became the most-watched program ever on Netflix in that country - and a package of MLB special events, including Opening Night and the Home Run Derby.

The event that best illustrates the economics was the Jake Paul vs. Mike Tyson fight in November 2024. It drew an average-minute audience of 108M live viewers globally, or 125M including the following day, peaked at 65M concurrent streams, and became the most-streamed sporting event ever, landing as the number-one title on Netflix in 78 countries.

The reported cost was around $60M in fighter purses.

Netflix added 18.9M net subscribers that quarter, more than double what analysts expected, with the company crediting the fight and the NFL games as major drivers. On a per-subscriber basis, that implied a customer acquisition cost near $3 per new member, compared with the $15-30 that large digital advertisers typically pay to acquire a customer.

Sports - especially live sports, and especially around major events - tap into some of the most deepest instincts in human behavior: anticipation, tribalism, scarcity, and the fear of missing out (FOMO).

That isn’t unique to Netflix. But Netflix understood how to position itself in the category, focusing on eventized sports rather than committing blindly to expensive, full-season rights packages.

And if the early results are any indication, live sports could become a much larger pillar of Netflix’s engagement, acquisition, and advertising strategy over time.

9. Gaming:

Netflix doesn’t disclose gaming revenue, largely because most titles are included within the subscription and have no in-app purchases. As a direct revenue line, gaming is effectively immaterial today. Management has also been clear about this: on the Q3 2023 call, co-CEO Greg Peters described Netflix’s scale and investment in games as “very, very, very small” relative to overall content spend and engagement.

For now, the objective isn’t revenue, but engagement and retention.

Netflix sees gaming as a way to compete for time, extend its franchises beyond passive viewing, and create new touchpoints around major IP. Titles such as Squid Game: Unleashed, launched around the show’s final season, illustrate the strategy: games can deepen fandom, support acquisition, and increase the lifetime value of successful franchises.

The strategy also appears to be shifting from mobile-only toward a more TV-based, cloud-first approach, with party-style games, kids experiences, and World Cup-related titles designed for the living room.

Netflix’s gaming strategy makes one thing increasingly clear: the competition is no longer just for subscribers, but for attention and time spent.

Netflix isn’t competing only against other streaming services. It is competing against TikTok, Facebook, Instagram, X, YouTube, linear TV, PlayStation, Xbox, and countless other forms of digital entertainment.

Found this content valuable? Leave a restack and like this article. These small actions go a long way in helping more people discover our work.

10. Short-form Videos: Netflix Clips

What could be more effective at retaining attention than short-form video?

Seeing the threat from TikTok, Instagram Reels, and YouTube Shorts, Netflix also moved in that direction. In April 2026, the company launched Netflix Clips.

Clips is a vertical, swipeable video feed inside Netflix’s redesigned mobile app, initially rolling out across 9 markets, including the US, UK, Canada, India, and Australia. The format is clearly inspired by TikTok, Reels, and Shorts: short, personalized, portrait-mode snippets from Netflix’s own films, series, and specials, with the option to save a title to My List, share a clip, or jump directly into the full episode.

Netflix, however, isn’t trying to build a social network or an infinite feed of user-generated content…

Clips is deliberately capped, and every clip is designed to push the viewer back into Netflix’s long-form catalog. CPTO Elizabeth Stone described the product as an experience for “the moments in between”: the commute, the lunch break, the wait at the airport.

That’s precisely the device and daypart where Netflix has historically been weakest - and where TikTok, Reels, and Shorts are strongest.

Clips is not a new revenue line today. It is a discovery and retention tool aimed at closing Netflix’s mobile attention gap.

Like gaming, it doesn’t monetize directly yet, although management has signaled that vertical video will eventually carry advertising, with ads in the format expected to roll out globally in 2027.

11. Advertising:

Advertising, once seen as a “desperate” attempt to reaccelerate the business, has proven to be one of Netflix’s most important expansion vectors - on two fronts: (i) bringing in new users and (ii) monetizing the existing base through ads.

The scale today is already substantial…

Netflix now has more than 250M monthly active viewers globally (not necessarily on the ad tier), and more than +80% of them watch content weekly. The ad-supported plan now accounts for more than 60% of new sign-ups in the countries where it is available, and Netflix plans to expand advertising into 15 new countries in 2027 (vs. 12 ad markets current).

Advertising revenue is currently around $1.5B and is expected to double to $3B in 2026. Some sell-side models already project more than $5B in 2027.

The biggest change, however, is infrastructure.

Netflix has built its own ad-tech backend, Netflix Ads Suite, replacing the 3rd-party platform it initially used at launch. That means the company now runs advertising directly on top of the richest content-engagement dataset in streaming.

It has also connected that inventory to programmatic demand through partners including Amazon DSP, Yahoo DSP, and The Trade Desk. In addition, Netflix made Omnicom Media its first data-collaboration partner, combining Acxiom audience data with Netflix’s AI-generated ad formats to place brand creative alongside relevant content and measure results in a closed loop.

Netflix cites internal figures of +44% incremental reach, meaning members seeing brands they wouldn’t have encountered on broadcast or rival streaming, about 2x the TV norm on long-term brand building, and results above benchmark on purchase intent.

Despite still being small relative to total revenue, at about 6%, advertising should carry a significantly higher gross margin than subscriptions.

Some may argue that this marks a departure from Netflix’s original value proposition - and there is some merit to that view. But from a business perspective, advertising is the clearest path for Netflix to grow back into a premium multiple.

It is still a multi-year story, and one the market doesn’t appear to be fully paying for today.

Enjoying the content? Upgrade to Jimmy’s Journal Pro to unlock the full experience - now with 25% OFF before prices increase in the next few days.

12. AI: Risk or Opportunity?

AI is a major revolution for content creation. We have already seen this at Meta, with short-form videos and ads on social networks, and at Adobe, with automated image generation.

For Netflix, it shouldn’t be any different - with one important caveat: video production is far more complex than what current models can replicate at scale.

Still, the fact is that AI tools are already being used inside the company.

In the Netflix original Argentine series The Eternaut (El Eternauta), the creative team needed a shot of a building collapsing in Buenos Aires - a visual effect that the show’s budget could not support through traditional VFX. Netflix’s in-house Eyeline Studios team built the sequence using AI-powered tools. On the Q2 2025 call, Ted Sarandos said the sequence was completed almost 10x faster than conventional VFX would have allowed, and at a cost that otherwise would not have been feasible for a production of that size.

The applications also extend to subtitles and dubbing. More than 30-35% of all viewing on Netflix now comes from non-English content, up from less than 10% a decade ago. Every one of those titles has to be dubbed and subtitled across dozens of languages, and AI-assisted dubbing and subtitling can reduce both the cost and the turnaround time of that work.

In discovery, the recommendation engine that already drives roughly 80% of viewing is being upgraded with GenAI for deeper content understanding, conversational search, and better promotional assets.

In advertising, the same first-party dataset now powers AI-generated ad formats that place brand creative inside the shows members are watching, a capability formalized through the Omnicom and Acxiom partnership.

And in M&A, the ~$600M acquisition of InterPositive, the AI filmmaking-tools company founded by Ben Affleck, signals that Netflix is willing to buy AI production capabilities rather than build all of them internally.

Despite these advances, we cannot ignore the risks that AI poses to Netflix’s business model. Reed Hastings himself has acknowledged that this may be the main risk to the thesis.

Netflix can certainly apply AI to the creation of its own content, but the bigger concern is that AI could eventually erode the scarcity on which Netflix’s entire model rests. If generative models make watchable, personalized video cheap enough for anyone to produce, the value of a $20B content budget and an exclusive library could decline.

13. Pricing Power and Churn:

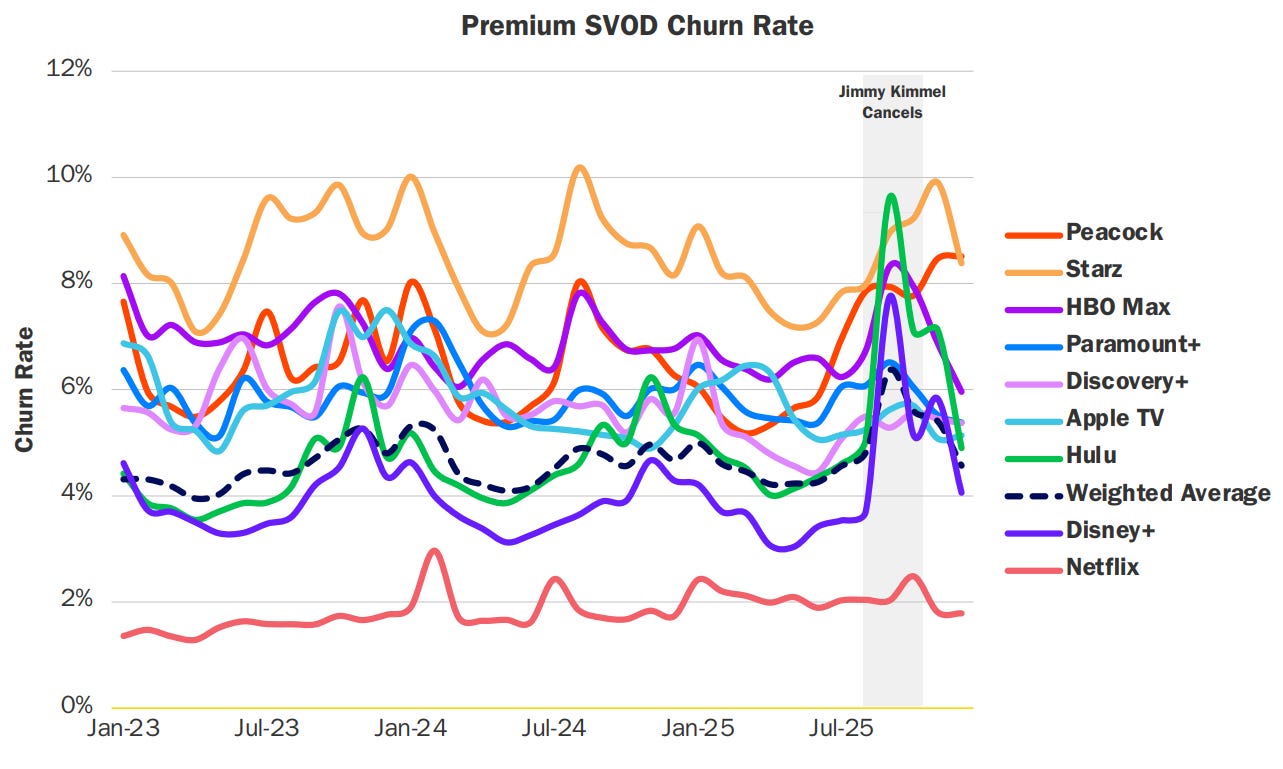

Despite the concentration risk and the constant need to find the next big show, churn is the metric that ultimately reveals the true strength of a streaming service - and Netflix has the lowest churn in the industry.

The industry today is divided into two groups: (i) Netflix, and (ii) everyone else.

Netflix’s churn sits at approximately 2% and has remained remarkably stable over the years, while the rest of the streaming industry continues to fight for retention with churn closer to 4.5-4.8%, with some services reaching as high as 8%.

Low churn is the engine behind the entire subscription model: it reduces the customer acquisition cost required to grow and gives Netflix the pricing power to push through repeated price increases over time.

And, of course, that’s exactly what it did, as shown below:

Found this content valuable? Leave a restack and like this article. These small actions go a long way in helping more people discover our work.

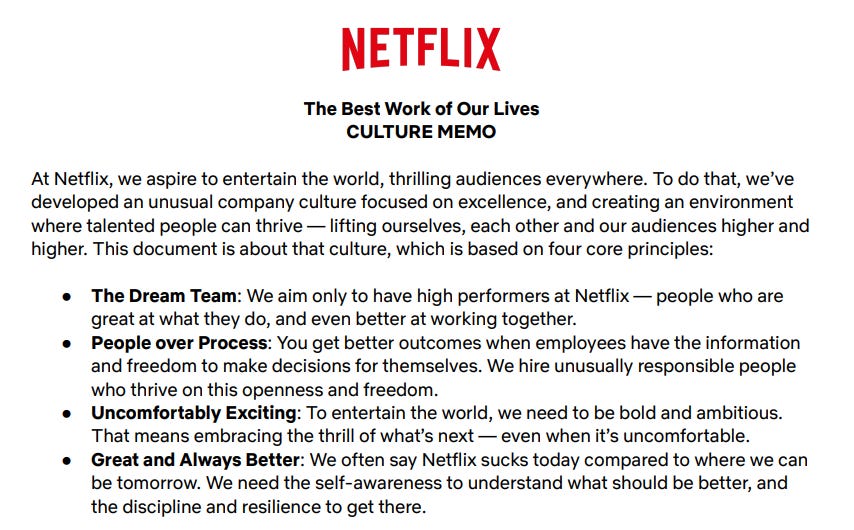

14. Culture: "No Rules Rules”

Netflix’s culture is unusually well documented.

It first became public through the 2009 “Netflix Culture” deck, which Sheryl Sandberg once described as one of the most important documents to come out of Silicon Valley.

It was later expanded by Reed Hastings and INSEAD professor Erin Meyer into the 2020 book No Rules Rules, which I highly recommend.

•")

The entire operating philosophy is built around one objective: keeping the company innovative enough to reinvent itself before someone else does.

A few principles sit at the core of that culture and help explain why Netflix has remained a company in constant evolution:

The first is talent density. Hastings’ framing is that “a great workplace is stunning colleagues.” A small team of exceptional people beats a large team of merely good ones because high talent density allows the company to remove the rules that average performers usually require.

The second is candor. Feedback at Netflix is expected to be continuous, direct, and part of the normal operating rhythm, not something reserved for annual reviews or moments of crisis.

The third is the removal of controls, captured by the phrase “lead with context, not control.” Netflix famously eliminated its vacation policy, its expense approval process, and most traditional sign-offs, replacing them with a single instruction: act in Netflix’s best interest.

The fourth is the enforcement mechanism behind the entire system: the “keeper test”. Managers are expected to ask themselves which people they would fight to retain. Those who don’t clear that bar receive what the company calls a generous severance package because, in Hastings’ own words, “adequate performance gets a generous severance package.”

In Hastings’ view, Netflix is a sports team, not a family.

Hastings’ thesis is that most corporate rules exist to prevent mistakes.

That’s the right objective in a factory or an airline, where errors can be catastrophic. But it’s the wrong objective in a creative business, where the cost of missing the next major hit can be far greater than the cost of making a mistake.

So Netflix deliberately trades control for freedom in order to maximize innovation and speed.

This may sound like a nice slogan to put on the wall, but at Netflix it has been actually applied in practice.

It is one of the clearest explanations for why the same company has managed to reinvent its core business several times: from DVDs to streaming, from streaming to originals, from a domestic service to a launch in 130 countries at once, and now into advertising, live sports, and games.

Each of those pivots cannibalized the model that came before it.

A culture optimized for error prevention would have protected the old business every time. A culture optimized for reinvention destroyed it on purpose.

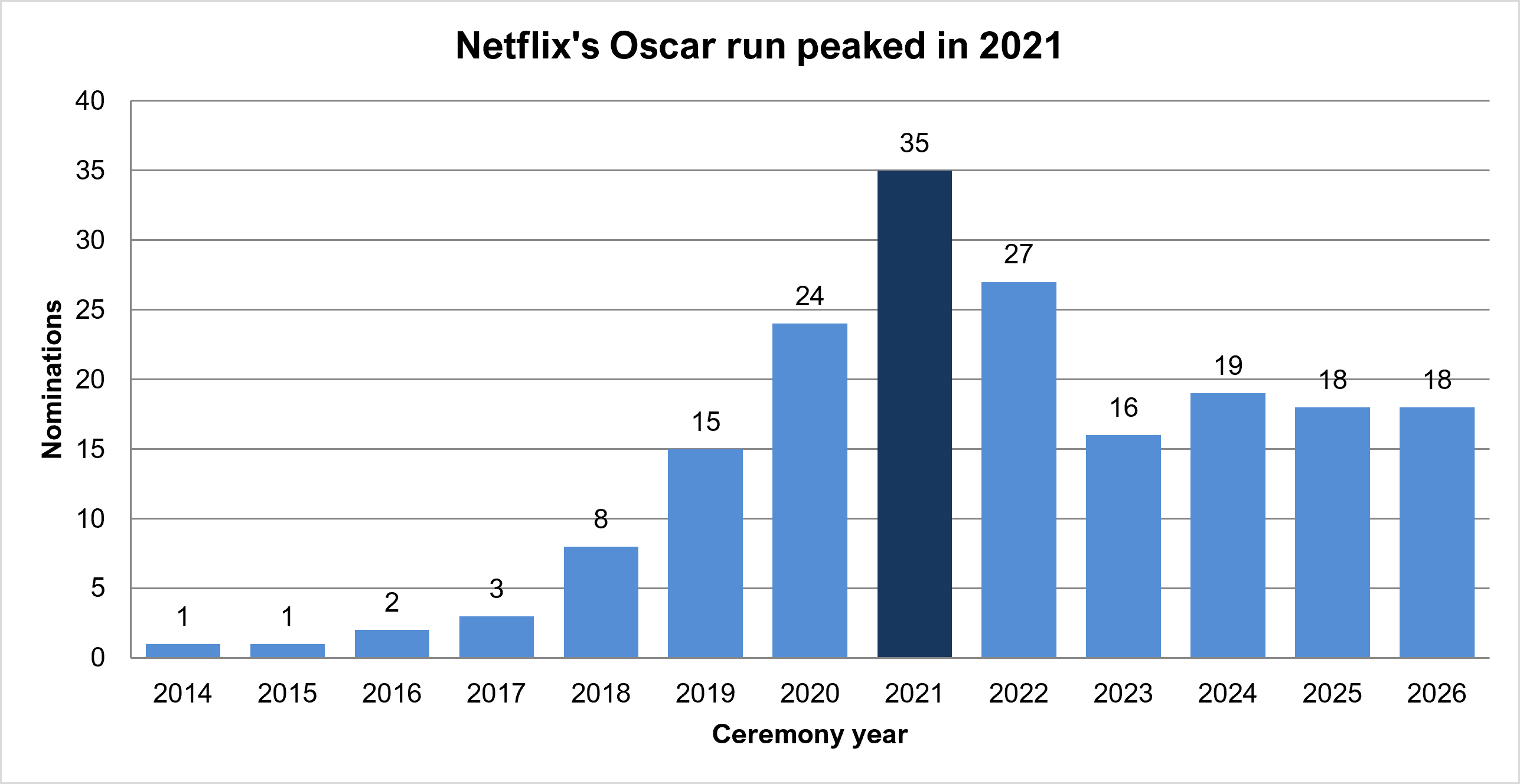

And nowhere is this more visible than in the awards circuit…

Since its first Academy Award nomination in 2014, for the documentary The Square, Netflix has won 33 Oscars, including 7 at the 2026 ceremony - tying its own single-year record and making it one of the most-decorated distributor by volume that night (Warner Bros won 11).

It has also won more than 260 Primetime Emmys.

Netflix achieved this without relying on the theatrical-first model that the industry had long treated as a prerequisite for prestige. Instead of releasing films primarily through cinemas first, Netflix put them directly in front of hundreds of millions of households.

This is one of the points Ted Sarandos has defended most aggressively. He has argued repeatedly that a wide theatrical window is an outdated requirement for most films, and that Netflix can reach a far larger audience through its platform than most titles ever could through a traditional cinema run.

The Academy has partly agreed and partly resisted.

Netflix now wins across animation, craft, documentary, and international categories. Despite 12 nominations for Best Picture, it still hasn’t won the industry’s most prestigious award, yet.

And despite peaking in 2021, Netflix has remained the studio with the highest number of nominations year after year.

15. Competitive Advantages:

Netflix couldn’t have emerged from the first wave of the Streaming Wars in such a strong position without a deep arsenal of competitive advantages.

In my view, Netflix’s moat rests on five main pillars:

The first is an unmatched value proposition. While competitors like Amazon, Disney, and Apple have multiple business lines competing for management attention, Netflix dedicates 100% of its efforts to improving the digital entertainment experience.

The company isn’t managing a transition away from legacy assets, protecting declining cable networks, or balancing streaming against theme parks, devices, or e-commerce. Netflix is a pure-play entertainment platform.

The second is the scale of its content spend. Netflix can spend more on content than almost any single competitor and amortize that investment across the largest paying audience in the world. Its owned productions IP, from Stranger Things to The Crown, create exclusive branding assets, attract top creative talent, and give users a reason to remain inside the Netflix ecosystem.

The third is differentiated technology. Netflix’s recommendation and data systems help retain members, increase engagement, and de-risk the content budget by improving the company’s ability to decide what to produce, license, or promote.

That same data layer is now becoming advertising infrastructure, allowing Netflix to target, measure, and monetize attention more effectively. On top of that, the company’s best-in-class product experience ´- from personalization and A/B testing to compression technology and its proprietary content-delivery network - keeps the service fast, reliable, and efficient at global scale.

The fourth is the brand. Netflix has become synonymous with the category itself. That reduces customer acquisition costs, supports pricing power, and helps explain why churn remains structurally lower than peers - around 2%, versus 4.8% for the industry average.

The fifth is culture. Netflix’s operating culture, which we will discuss next, is one of the company’s least visible but most important advantages. It allows the business to move faster, maintain higher talent density, make harder decisions earlier, and ultimately deliver superior margins versus the rest of the industry.

Enjoying the content? Upgrade to Jimmy’s Journal Pro to unlock the full experience - now with 25% OFF before prices increase in the next few days.

16. M&As & Capital Allocation:

M&As:

Netflix’s M&A history is very short, which is exactly what makes 2026 so significant.

For most of its life, Netflix built rather than bought. Its acquisitions were small and strategic: a comics studio in Millarworld, the Roald Dahl Story Company, a handful of game developers, and a few VFX and animation assets. The philosophy was that organic content creation, paired with a superior product and global distribution, was cheaper and more effective than buying someone else’s legacy assets.

That philosophy changed in 2026.

Netflix bid for Warner Bros. Discovery’s studio and HBO Max streaming assets, deliberately excluding the declining cable networks. Its final offer was $27.75/share in cash, valuing those assets in the $80B range.

For a company that had spent 20 years insisting it didn’t need to buy scale, this was a major strategic departure.

When Paramount Skydance, backed by Larry Ellison’s capital, escalated to $31/share in cash for all of WBD, Netflix refused to raise its bid. It walked away and collected a $2.8B break fee, which Paramount agreed to fund.

That fee flowed through Netflix’s first-quarter results, inflating reported EPS to $1.23 and boosting free cash flow.

If the market previously had doubts about management’s discipline in capital allocation due to the lack of a long M&A track record, those doubts should now be much smaller.

Netflix was willing to pursue a transformational acquisition, but it wasn’t willing to overpay for it.

Still, the episode leaves behind a few important signals worth analyzing.

A company that seriously considers an $80B acquisition is also a company whose leadership may see the organic S-curve flattening enough to at least consider buying growth - or buying the content-production capacity, franchises, and IP that WBD’s studio would have provided.

You don’t spend 18 months pursuing an $80B studio if you are fully confident that your own content engine alone can sustain 15-20% growth for another decade.

The InterPositive deal, small as it is, points in the same direction. Netflix is now willing to buy capability - in this case, AI production tools - rather than build everything internally.

Shareholder Return:

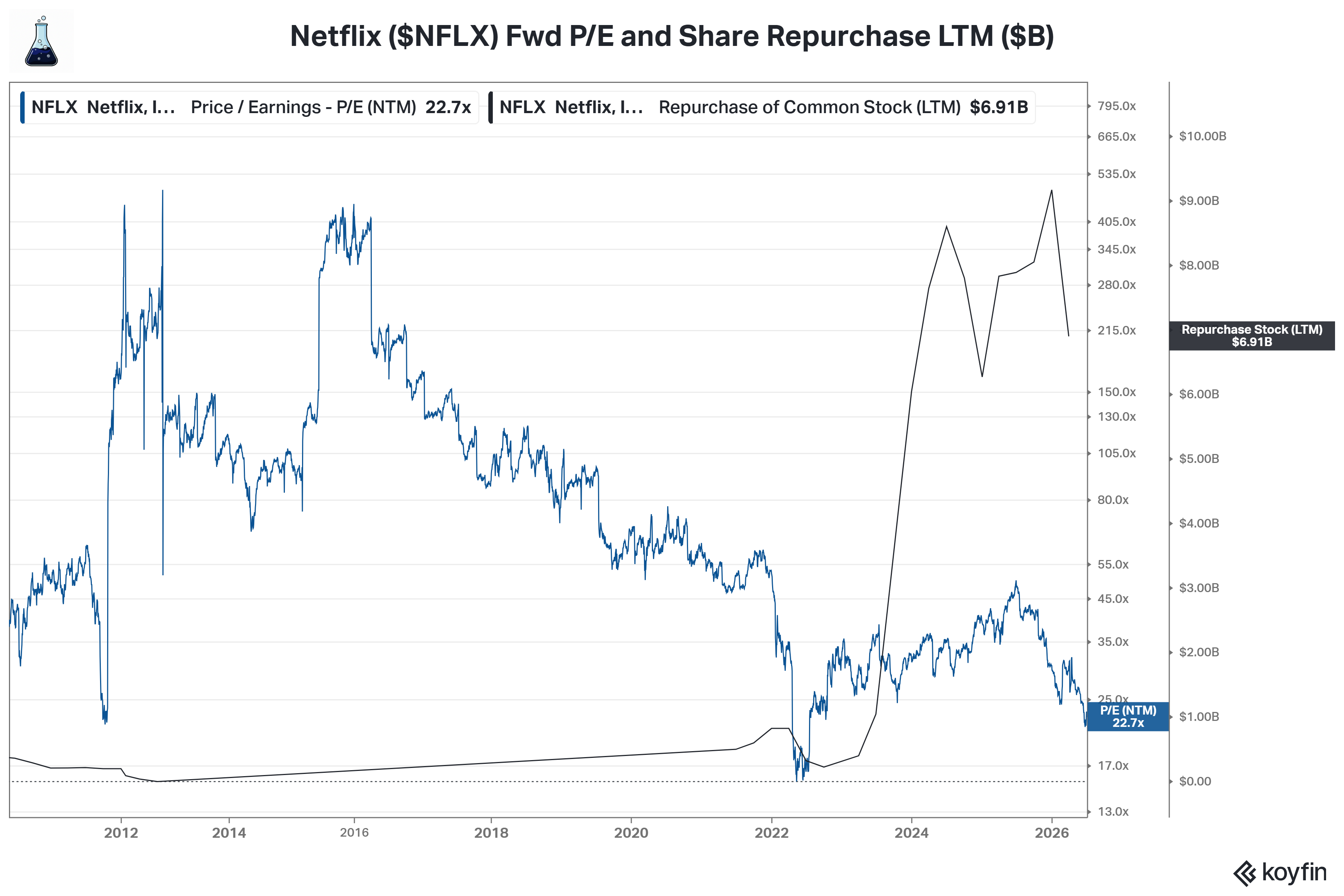

The company has never paid a dividend, with buybacks serving as the primary mechanism for returning capital to shareholders.

Over the last 12 months, Netflix has repurchased more than $6.9B (~2% of market cap), at a forward P/E multiple close to 25-28x - a detail that says a lot about the company’s capital allocation discipline.

17. Corporate Governance:

Reed Hastings’ Succession:

Netflix was a founder-led company until very recently, and I must admit that I have rarely seen a leadership transition as well structured as Reed Hastings’ succession.

As mentioned earlier, Hastings had been at the center of the company since its founding in 1997. The transition effectively began in 2020, when he elevated Ted Sarandos to co-CEO, and continued in 2023 with the appointment of Greg Peters as co-CEO. The dual-CEO structure - Sarandos leading the content and creative side, Peters bringing the product, technology, and operating lens - has worked smoothly through a period of enormous strategic change.

Reed left the board at the June 2026 annual meeting after nearly 30 years with the company to focus on philanthropy, and the standard “no disagreement with the company” language appears genuine. Netflix later named Jay Hoag, a longtime venture investor and director since 1999, as chairman of the board to replace Hastings.

He is the same director shareholders had effectively voted against at the 2025 annual meeting, after he failed to receive a majority of votes cast for his reelection. Netflix attributed the vote mainly to his 2024 attendance record, while also noting that he had attended 97% of meetings over the prior 5 years. The board rejected his offered resignation in June 2025 and kept him on as lead independent director. One year later, shareholders reversed course, reelecting him with broad support, and the board elevated him to chairman following Hastings’ departure.

Main Directors:

After the reorganization, Netflix’s operating leadership is anchored by four key executives:

Ted Sarandos, co-CEO and President, remains the company’s creative and content leader. He has overseen Netflix’s content operations since 2000 and led the company’s move into original programming beginning in 2013 with titles such as House of Cards, Arrested Development, and Orange Is the New Black.

Greg Peters, co-CEO and President, brings the product, technology, and operational side of the company. Before becoming co-CEO in 2023, he served as COO and Chief Product Officer, and previously helped lead Netflix’s international expansion.

Spencer Neumann, CFO since 2019, is the financial anchor of the model. His background across Disney, Activision Blizzard, and private equity is particularly relevant for a company now balancing content investment, margin expansion, advertising, buybacks, and potential M&A.

Bela Bajaria, Chief Content Officer since 2023, oversees Netflix’s global content machine across series, films, live events, and sports. Her role is central to the company’s biggest strategic question: how to keep the content engine productive enough to sustain engagement and justify the scale of Netflix’s annual content spend.

Board:

The board now consists of 12 directors, several of whom are particularly notable.

Jay Hoag, Chairman, has served on Netflix’s board since 1999. He is a founding general partner of TCV and one of Netflix’s earliest institutional investors.

Ted Sarandos and Greg Peters, the company’s two co-CEOs, also serve as directors.

Richard Barton is the co-founder of Zillow, Expedia, and Glassdoor.

Leslie Kilgore is Netflix’s former Chief Marketing Officer and the executive behind the internal phrase “act in Netflix’s best interest.”

Ann Mather is the former CFO of Pixar and an experienced technology board member.

Brad Smith is Vice Chair and President of Microsoft.

Ellie Mertz, Airbnb’s CFO and a former Netflix executive, joined the board in June 2025.

Found this content valuable? Leave a restack and like this article. These small actions go a long way in helping more people discover our work.

18. Financials:

We have already touched on Netflix’s financials throughout this deep dive.

The company has a loyal customer base, low churn, and an increasingly predictable revenue stream. Advertising is now being layered on top of that same existing base, but with significantly higher incremental margins.

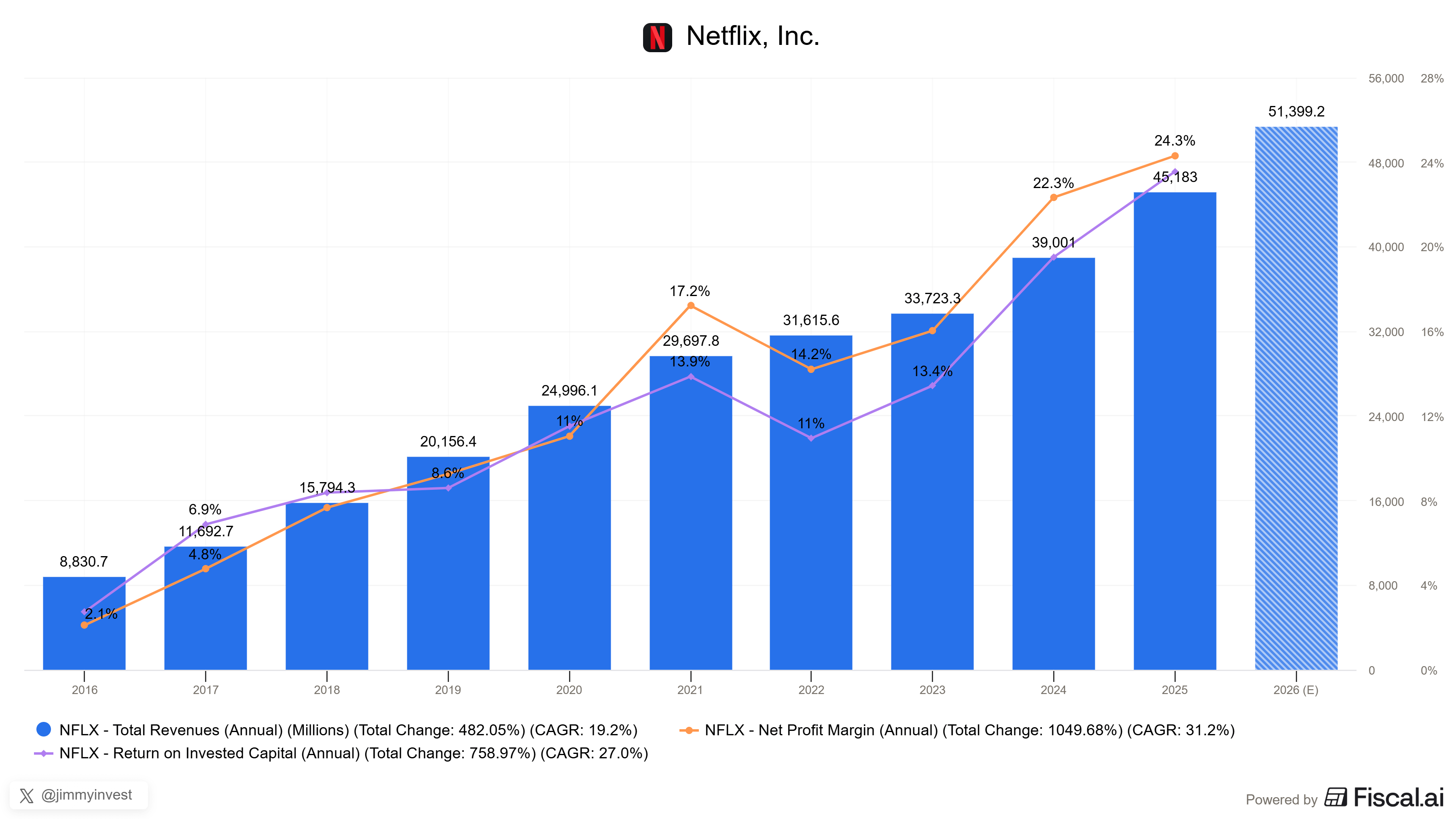

Over the last 10 years, net revenue grew at a 19.2% CAGR, reaching $45.1 billion in 2025. For 2026E, revenue is expected to grow another 13.7%.

In UCAN, higher ARPU should be the main source of incremental value, as subscriber penetration is already high.

In APAC and LATAM, the opportunity is broader, and Netflix can still expand the user base while gradually increasing ARPU through pricing, tier mix, advertising, and greater local-content penetration.

Net Margin, driven mainly by the dilution of content amortization across an increasingly larger customer base, expanded from 2.1% to 24.3% over the same period.

ROIC followed a similar trajectory, almost perfectly correlated with net margin, reaching 23.6% in 2025.

Management is guiding to a 31.5% Operating Mrg. for FY2026, up from 29.5% in 2025 and in line with the 31.2% reported in Q1 2026.

The balance sheet is also a fortress relative to traditional media peers. Gross debt sits around $14.4B against ~$12.3B of cash, implying non-GAAP net debt of only about $2.1B.

Content assets on the balance sheet are approximately $32B, while total streaming content obligations stand near $24B.

19. Valuation:

Multiples:

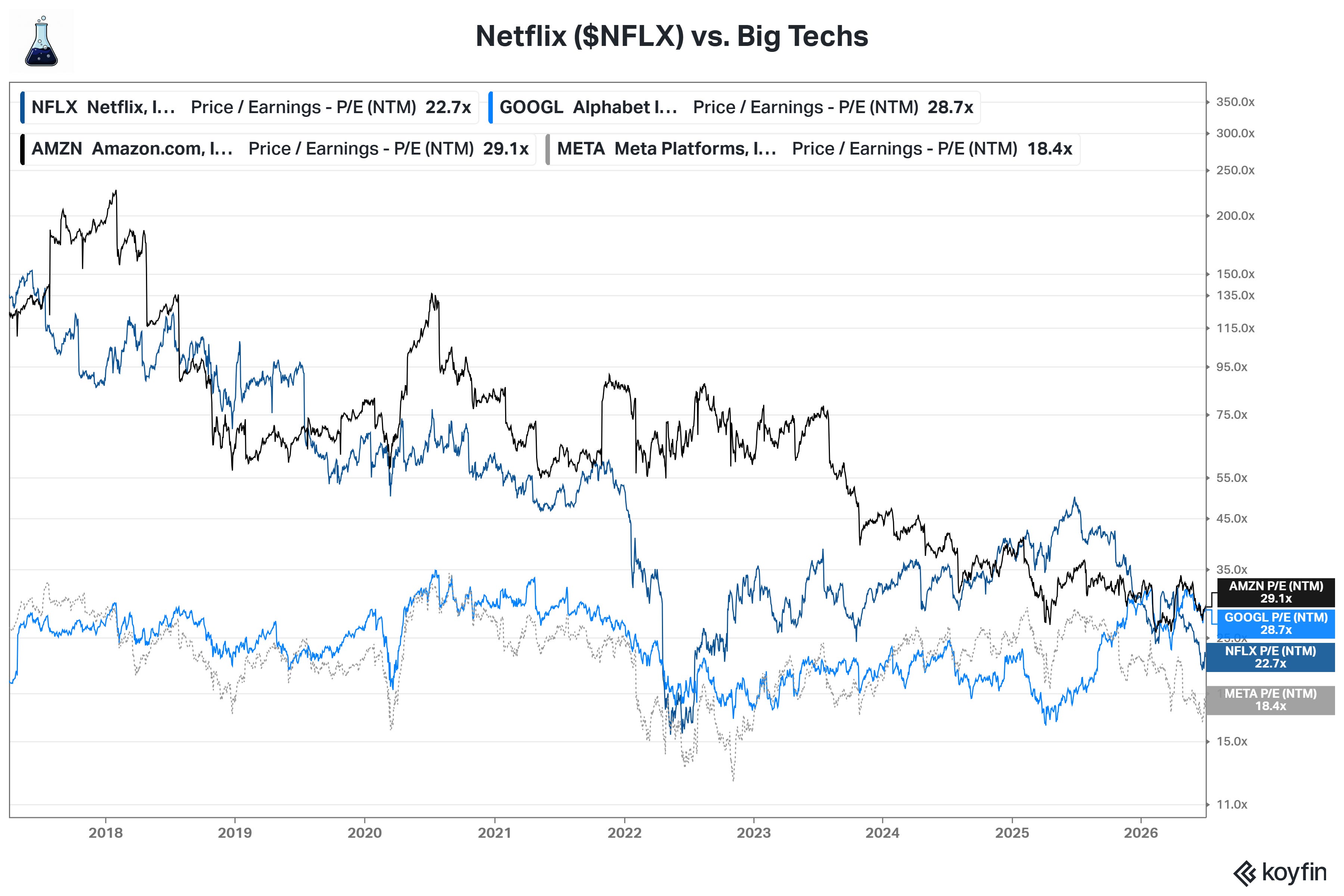

For most of the last decade, Netflix was priced as a technology compounder.

The stock routinely traded at 50x, 80x, and sometimes more than 100x forward earnings - and at even higher multiples during its earlier hypergrowth years. The premium was based on the belief that Netflix could keep compounding revenue at scale while expanding margins, much like the best software platforms.

Today, that once-deserved premium has largely disappeared.

Netflix now trades at 20x forward P/E based on our 2027E earnings estimate, and around 24-25x trailing P/E - near the low end of its history as a profitable company and well below its own multi-year average.

If we think about the old FAANG group, Netflix now trades broadly in line with the mega-cap technology companies, despite slightly faster bottom-line growth. The difference, of course, is that Netflix doesn’t benefit from the same direct AI upside that the market currently assigns to several of those names.

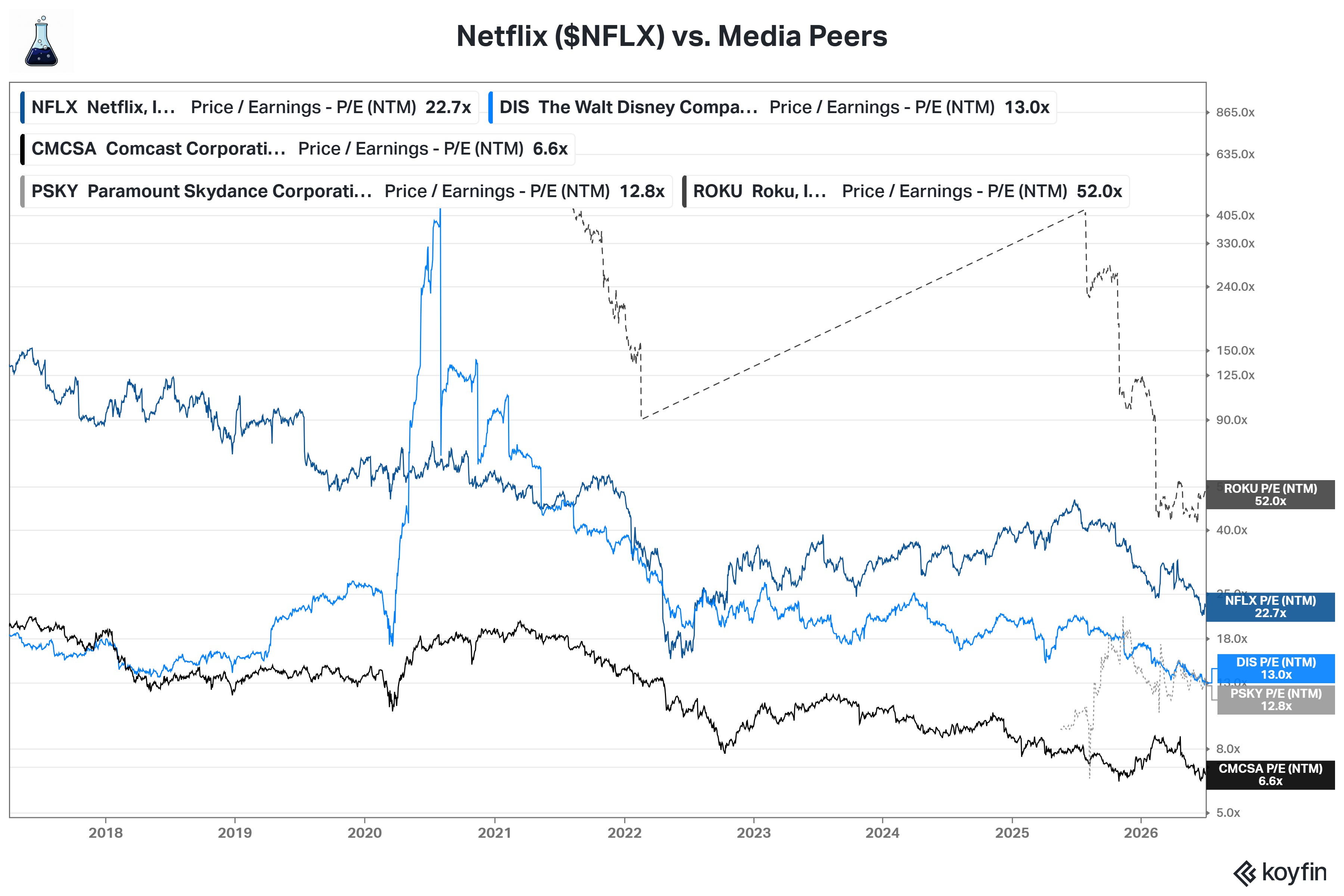

Against traditional media peers, however, the comparison looks very different.

Netflix trades at a significant premium to Disney, Comcast, and the consolidating Paramount-WBD complex.

In our view, that premium is fully justified.

Those companies are managing secularly declining assets, cutting content, restructuring balance sheets, and consolidating largely from a position of weakness.

Netflix, by contrast, is still growing, still expanding margins, and still consolidating attention from a position of scale.

But growing for how long? And how far can margins expand? These are the questions our DCF tries to answer in the next section…

From here on, this article is exclusive to paid subscribers.

If you want to secure access to Jimmy’s Journal Pro with 25% OFF, click the link below and subscribe before our price increases to $397/year in the next few days.

Discounted Cash Flow (DCF):

Since Netflix provided useful granularity on ARPU and membership by region until 2024, we will use those data points as the initial foundation for our model.