Teradyne ($TER) Deep Dive

Structural, or just another cyclical trade?

Hi, Investor! 👋🏼

I’m Jimmy, and welcome back to another edition of Jimmy’s Journal.

You have probably been following the recent rally in semiconductors…

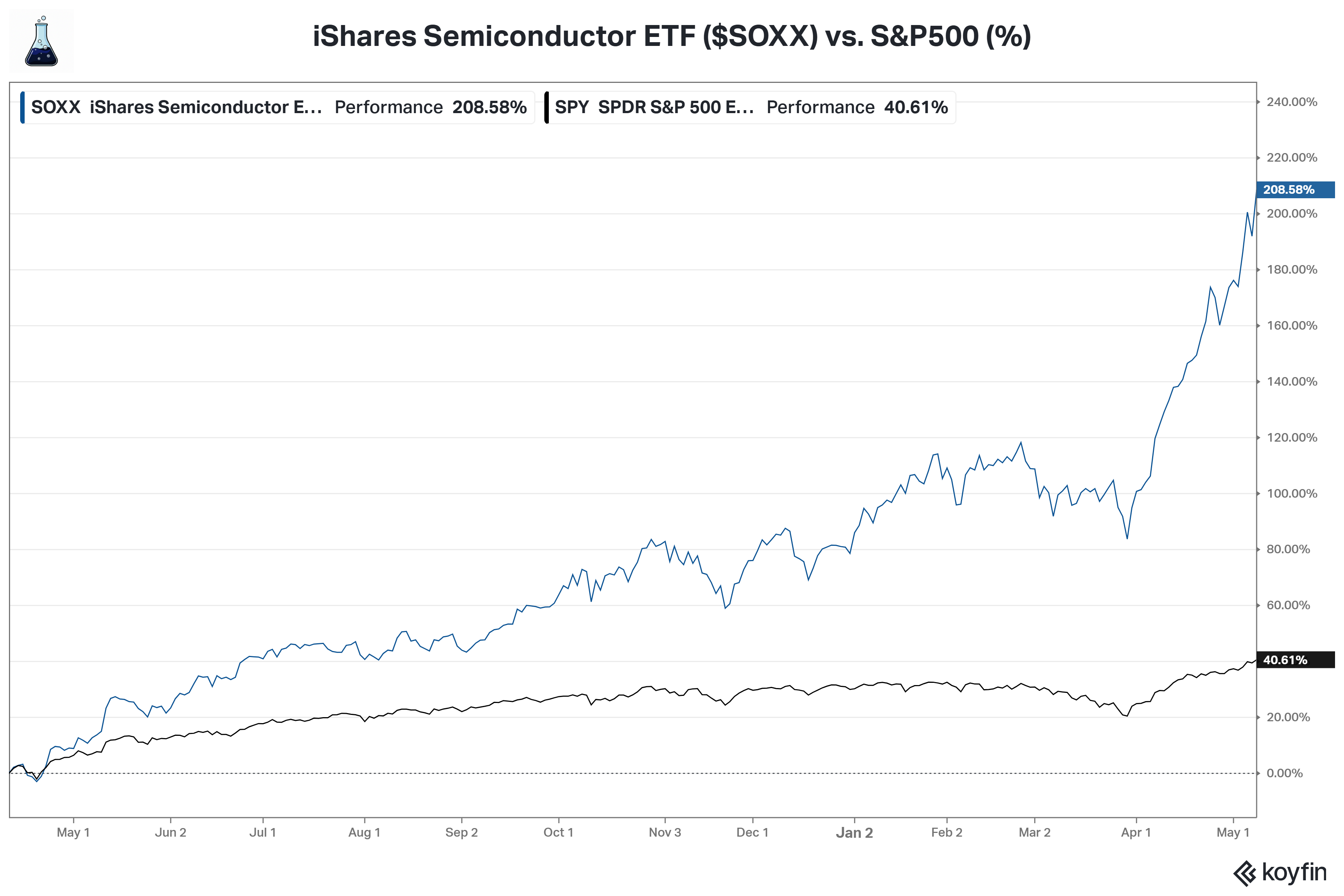

The iShares Semiconductor ETF (SOXX) has delivered a total return of approximately +200% over the past twelve months, making it one of the strongest single-sector runs in the past two decades.

The S&P 500, over the same period, returned a fraction of that.

The outperformance gap of well over 150 p.p. reflects what is happening at the structural level: every dollar of incremental AI capex flows, in some form, through the semiconductor value chain.

NVIDIA, Broadcom, AMD, TSMC, ASML. Those are the names everyone knows…

They design the chips, fabricate them, and supply the lithography that makes the whole thing possible.

But there is a quieter name sitting one layer underneath all of them, and it has compounded its way into one of the most critical pieces of infrastructure inside the most important industry of our time.

That name is Teradyne ($TER).

The company does not design chips, does not fabricate them, and does not package them.

But no chip leaves a manufacturer until a Teradyne tester (or one of its closest competitors) signals that it works as designed.

Every die, every wafer, every chip.

This is the gating step of the entire semiconductor value chain…

And the more complex the chip, the more critical the test step becomes.

Until recently, this business was understood as a textbook cyclical: capital equipment levered to mobile cycles, with predictable peaks tied to iPhone launches and predictable troughs in the years between.

That framing is no longer accurate…

Today, Teradyne sits at the intersection of multiple secular tailwinds at once: custom ASICs for hyperscalers, HBM and high-density memory, merchant GPU dual-sourcing, silicon photonics for co-packaged optics, and a Robotics segment with quietly accelerating growth.

Add to that the adjacent demand from data center buildouts, electrification, and the broader industrial automation cycle, and what was once a single-cycle story becomes a multi-vector compounding platform.

The numbers reflect this transformation:

On April 28, 2026, the company reported the best quarter in its 66-year history. Revenue of $1.28B, up +87% y/y. AI now accounts for nearly 70% of total revenue. The mobile peak of 2021 was surpassed by $200M in a single quarter.

The business is generating significant cash, the balance sheet is extremely healthy, and management is aggressively repurchasing shares at 55x earnings.

Which raises the question this deep dive exists to answer:

Is Teradyne the AI-infrastructure compounder that finally broke out of its mobile-cycle past, deserving of a structurally higher multiple? Or is it a still-cyclical capital equipment business priced for perfection at the worst possible moment?

What you are about to read is one of the most comprehensive deep dives I have published on Premium:

18 sections, more than 10,800 words of original analysis covering the duopoly with Advantest, the critical role Teradyne's testers play in the semiconductor production chain, the opportunities across ASICs, GPUs and memory, the company's moats, the long-term outlook, and our final rating.

The article is dense, so we have organized it as follows:

Investment Thesis

Industry Overview

Company History

Corporate Governance

Business Model

Semiconductor Tests

Value Proposition

Unit Economics

Competitive Landscape

Competitive Moats

The Cyclicality Question

The Merchant GPU Opportunity

VIP ASIC, HBM and Silicon Photonics

Capital Allocation and M&As

Financials and Long-Term Targets

Valuation

Risks

Final Thoughts

Already a Premium subscriber? Feel free to skip this section and jump straight to the full report below.

This article is exclusively available to Premium subscribers of Jimmy’s Journal.

Inside the full report, we break down:

Why the market may be mispricing Teradyne’s long-term AI exposure

Why semiconductor testing may become one of AI’s hidden bottlenecks

How silicon photonics could unlock a new multi-billion-dollar TAM

The competitive dynamics versus Advantest and emerging challengers

A complete valuation framework, including scenario analysis and downside risks

This is the type of institutional-quality research usually reserved for professional investors.

↳ Upgrade to Premium using the link below, avoid Apple/Google fees, and unlock the full thesis:

« Upgrade to Premium »

1. Investment Thesis:

Before we go deeper, here are the five pillars that sustain the bull case for Teradyne: