How to Spot Companies with Real Economic Moats

How to identify companies with sustainable competitive advantages using ROIC, margins and market share...

Hi, Investor 👋

I’m Jimmy, and welcome to another free edition 🔓 of our newsletter. Today, I’ll show you how to spot companies with real, lasting competitive advantages - what we call economic moats.

Stick with me - there’s a great bonus waiting for you at the end of the article. Let’s dive in.

In case you missed it, here are some recent insights:

Subscribe now and never miss a single report:

The concept of an economic moat, popularized by Warren Buffett, refers to a company’s ability to maintain its competitive edge over time - just like a medieval castle protected by a moat.

These are the kinds of businesses that can withstand competition, consistently generate above-average profits, and reinvest capital at high returns.

In a world where disruption is constant and margins are always under pressure, identifying companies with strong economic moats is one of the most effective ways to invest with a long-term mindset.

But what exactly constitutes a moat?

And how can investors recognize one before the rest of the market does?

The Foundation of a Moat:

A wide moat is built on one or more structural advantages that make it hard for competitors to replicate a company's success.

Replicate - this word is very important.

These advantages often fall into a few categories:

Network Effects: as more users join a platform, the product becomes more valuable (e.g., Uber, Visa, Facebook, or Microsoft Office).

Intangible Assets: this includes patents, brand equity, regulatory licenses, or proprietary technology (think Coca-Cola’s brand or Moody’s licenses).

Cost Advantages: companies that can deliver similar goods at a lower cost have more room to compete on price or margin (like Costco, Walmart or Home Depot).

Switching Costs: when it’s painful for customers to change providers, retention becomes much easier (e.g., Apple, Salesforce, Adobe or enterprise SaaS products).

Efficient Scale: in markets with limited demand, a few players can dominate and make it uneconomical for new entrants (such as regional utilities or railroads).

These moats not only help a company endure over time - they enable it to reinvest capital effectively, which is the ultimate goal for long-term investors.

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

Key Signals of a Moat:

Moats, by nature, are hard to quantify.

But we can find financial footprints that suggest the presence of a durable competitive advantage. Let’s explore three quantitative signals:

1. Sustained High Return on Invested Capital (ROIC):

ROIC measures how effectively a company turns invested capital (both debt and equity) into profit. In competitive markets, ROIC tends to fall as competitors flood in and erode margins.

However, companies with moats can maintain high ROIC even under pressure. Think of it as a litmus test for durability.

For example, software companies with sticky products and low marginal costs (like Intuit or Autodesk) often post high ROIC for extended periods. A consistent ROIC above 15% is a strong sign the company can reinvest earnings at attractive rates - fueling long-term intrinsic value growth.

2. High and Stable Gross Margins:

Gross margin reflects a company’s pricing power and cost efficiency. A firm that can consistently charge more than it costs to produce goods has room to invest in R&D, marketing, or customer retention - while still posting strong profits.

However, it’s not just about high gross margins - it’s about stability. A business with volatile margins might be exposed to commodity costs or cyclical forces.

On the other hand, a company that posts 60%+ gross margins year after year, even through downturns, probably has a moat worth investigating.

3. Dominant Market Share:

Owning a large share of a niche or fragmented market can reflect competitive dominance. This could be the result of scale, brand loyalty, or strong distribution channels.

For example, Google ($GOOG) commands over 90% of the global search market. This scale enables massive data advantages, pricing leverage with advertisers, and network effects that make it nearly impossible to disrupt.

Of course, high market share isn’t always a moat - especially if the product is a commodity. Airlines are a good example: a few players dominate, but low pricing power and high capital costs make the business unattractive.

Moats in Practice: Real-World Examples

Let’s look at a few companies with enduring moats and the traits that support them:

Apple (AAPL): combines brand power, switching costs (ecosystem), and pricing power. Its gross margins and ROIC are consistently high, and customer loyalty is unmatched.

Costco (COST): operates with razor-thin margins but leverages its scale and membership model to create customer lock-in. It passes savings on to customers and retains trust.

Visa (V): a classic network effect play. Every new user or merchant on the platform makes the network more valuable. It's capital-light and generates immense free cash flow.

Microsoft (MSFT): benefits from both switching costs (Office, Azure) and brand trust in enterprise environments. Its reinvestment strategy into cloud and AI shows how moats evolve.

Enjoying the content? Encourage me to keep creating more like this. Buy me a coffee!

The S&P 500 Economic Moat Index:

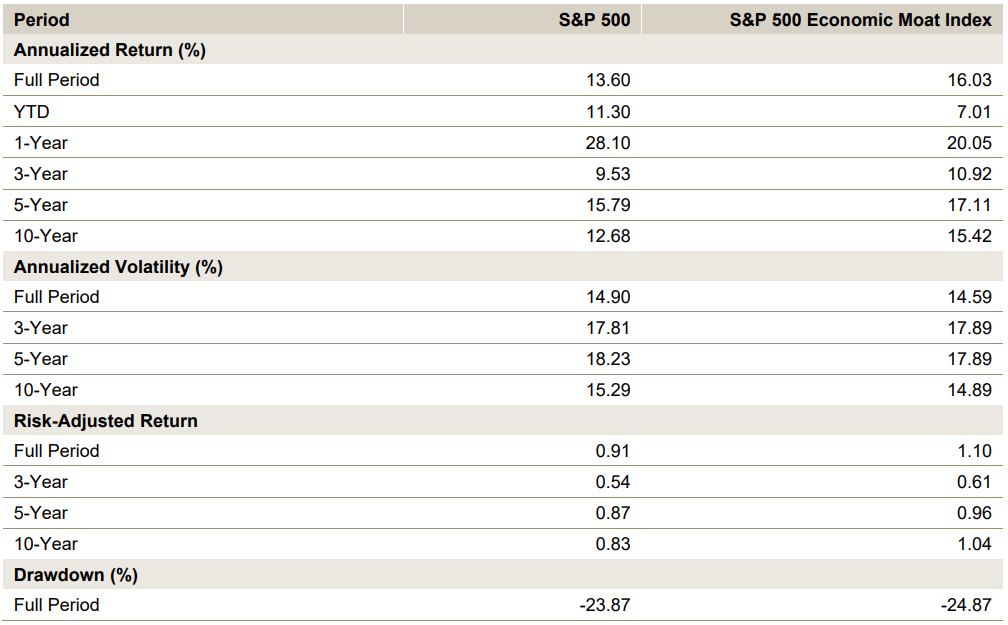

In my search for studies focused on companies with durable competitive advantages, I came across the S&P 500 Economic Moat Index - launched in April 2024.

This index aims to measure the performance of companies with strong and sustainable moats, using a purely quantitative framework.

Rather than relying on subjective analyst opinions, it selects 50 companies based on clear indicators:

5-year average ROIC

5-year average and stability of gross margins

Relative market share in their respective industries

What’s notable is that this quantitative approach has delivered higher risk-adjusted returns (+16,03%) with lower volatility (14,59%) than the broader S&P 500 in the last 10 years:

The index shows that consistent profitability and competitive dominance aren’t just theoretical - they translate into long-term outperformance.

1. Profitability Comparison:

A wide economic moat gives a company the ability to protect its margins and generate consistently strong profits - one of the clearest indicators of business quality.

Over time, companies with these advantages have outperformed the broader market across key metrics such as return on equity (ROE), return on invested capital (ROIC), and return on assets (ROA), reflecting their superior ability to allocate capital efficiently and sustain profitability.

Interestingly, the S&P 500 Economic Moat Index captures 102% of the market’s upside during rallies, while only participating in 88% of the downside during market declines.

In other words, it benefits from return compounding over time - going up more when the market rises, and falling less when the market drops.

2. Composition Comparison:

It’s interesting to note how closely the composition of the S&P 500 Economic Moat Index aligns with what we observe in the real world.

If I asked you which sectors tend to have the fewest competitive advantages, you'd probably say:

Commodities (Materials and Energy);

Real Estate; and

Airlines.

And that’s exactly what the index reflects - these sectors are significantly underrepresented.

On the other end of the spectrum? No surprise there...

Consumer Discretionary;

Consumer Staples; and

Information Technology.

These sectors often benefit from powerful competitive advantages like strong brands, network effects, and high switching costs.

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

Why Moats Matter More in Volatile Markets:

In bull markets, almost everything goes up - investors often chase stories, not fundamentals.

But during recessions, inflation shocks, or rate hikes, companies with weak economics suffer disproportionately.

Those with strong moats, however, tend to hold their ground.

Moats provide resilience.

Companies with pricing power can pass on cost increases. Firms with sticky customers won’t see revenues evaporate overnight. And those with strong balance sheets (often a byproduct of efficient capital use) can weather storms without dilutive equity raises or excessive debt.

In short: moats act as shock absorbers in your portfolio.

What to Avoid:

Just because a company has high margins or market share doesn’t guarantee a moat. Be cautious of:

Cyclical peaks: high ROIC in commodities or real estate during upcycles can be misleading.

Fads and hype: temporary business models with no clear long-term edge.

Debt-fueled growth: a company generating good returns now but burning cash or over-leveraging to grow.

Moats must be sustainable.

Look for consistency across time and across metrics - not one good year.

Enjoying the content? Encourage me to keep creating more like this. Buy me a coffee!

Before You Go: Final Notes (+ Jimmy’s Bonus 🎁)

Economic moats aren’t always obvious - but they are measurable.

By focusing on durable profitability, pricing power, and competitive dominance, investors can tilt their portfolios toward quality and resilience.

In a market obsessed with momentum and short-term results, moats offer something far more valuable: compounding power with protection.

As Warren Buffett once said,

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage.”

If you’re looking to deepen your understanding of competitive advantages - and ultimately boost your long-term returns - here are two outstanding reading recommendations:

1. Measuring the Moat – Michael Mauboussin (white paper)

One of the most insightful technical studies on how to quantify and interpret competitive advantages using financial data such as ROIC, gross margins, and invested capital.

2. Competition Demystified: A Radically Simplified Approach to Business Strategy – Bruce Greenwald

The best book on competition I’ve ever read (far more practical than Jim Collins or even Michael Porter). It explains what truly keeps a company on top over the long run.

What about you? Which companies in your portfolio meet the criteria above?

Drop a comment - I’d love to hear your thoughts.

Cheers,

Jimmy

Disclaimer

As a reader of Jimmy’s Journal, you agree with our disclaimer. You can read the full disclaimer here.

Great content! 👏🏼👏🏼