Top-5 Out-of-Consensus Investment Ideas for 2025

Unconventional opportunities the market is overlooking in 2025...

Hi, Investor 👋

I’m Jimmy, and welcome to another edition of our newsletter. Today, we’re exploring 5 out-of-consensus investment ideas for 2025 - opportunities the market may be overlooking but have the potential for strong long-term returns.

Hope you enjoy the insights! Don’t forget to share with friends and fellow investors.

In case you missed it, here are some recent insights:

Subscribe now and never miss a single report:

"Consensus thinking leads to consensus returns. True alpha comes from differentiated insights." - Michael Mauboussin

Inspired by this quote from Michael Mauboussin, I’m sharing a few out-of-consensus investment ideas for those looking to outperform the market.

These are not my personal investments (those are covered in the Stellar Capital Management series), but I see the following stocks as strong opportunities for investors seeking to think differently.

In total, there are five, all with a market cap below $100B...

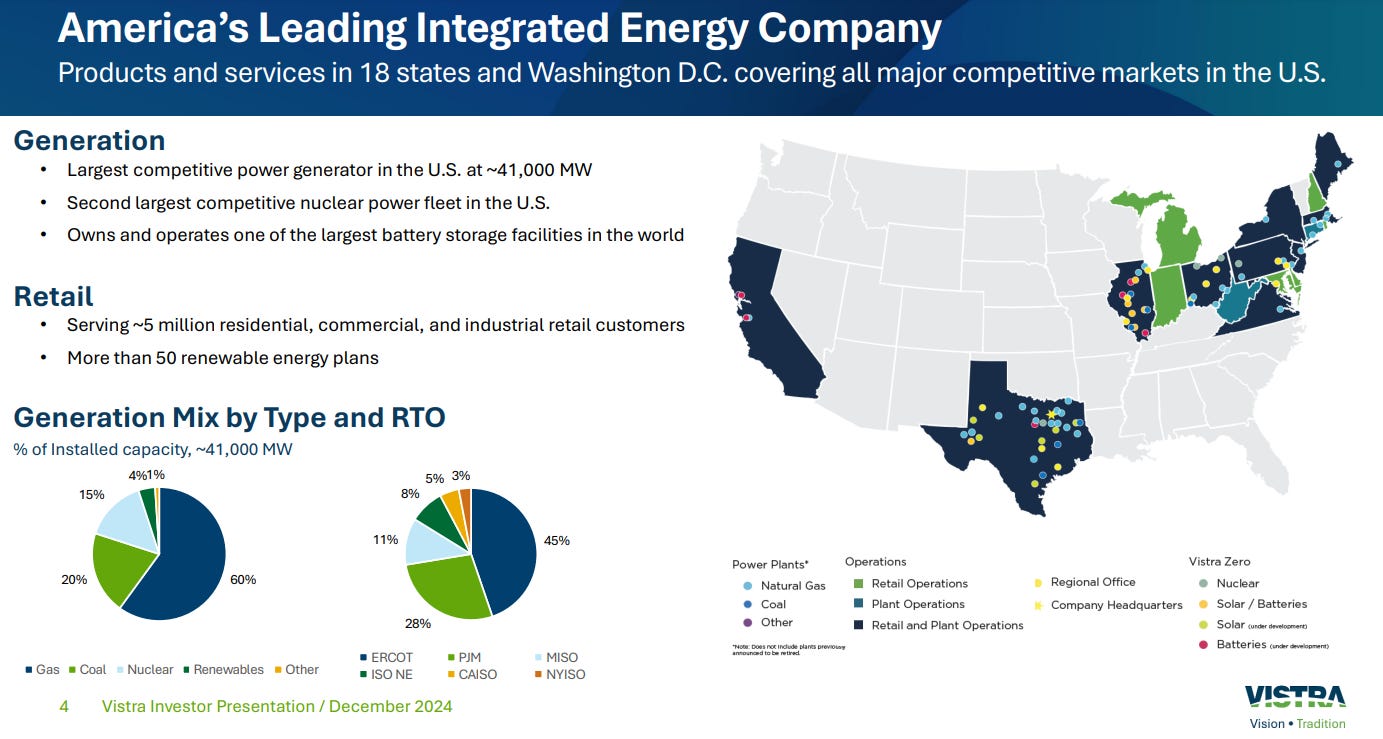

5. Vistra Corp (VST):

Business Model:

Vistra is a leading integrated power producer with significant exposure to ERCOT, benefiting from the structural tightening of the Texas power market. With a diverse generation mix spanning natural gas, nuclear, and renewables, the company is well-positioned to capitalize on rising electricity demand, intra-day price volatility, and base load growth.

Beyond ERCOT, Vistra’s strategic optionality in gas and nuclear PPAs provides additional upside. While exact timing around new contracts remains uncertain, successful agreements could serve as a near-term catalyst for shares. Longer-term, Vistra’s ability to secure new gas plant contracts could enhance cash flow stability, as large power users compete for reliable supply amid growing electricity demand.

Why is Vistra interesting?

High ERCOT Exposure: Positioned to benefit from tightening power supply and demand growth in Texas.

Gas & Nuclear PPA Upside: Potential for long-term contracts to improve cash flow visibility.

Power Market Optionality: Ability to capitalize on price volatility and base load demand increases.

Valuation:

Vistra trades at a forward P/E of 22x, reflecting strong earnings momentum as power demand rises. The company maintains a 12% net margin, supporting consistent profitability, and a 3.55% free cash flow yield, highlighting its ability to generate solid cash returns.

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

4. Crown Holdings:

Business Model:

Crown Holdings (CCK) is the second-largest aluminum can producer globally, holding a 20% market share, just behind Ball at 26%. The company generates $8.4 billion in beverage can sales, about three-quarters of Ball’s revenue, while maintaining a higher return on assets (13.5% vs. 11.0%). Crown’s business benefits from global expansion initiatives, strong demand for consumer soft drinks, and lower exposure to domestic beer, positioning it for above-average volume growth in 2024.

Crown's capital efficiency and strategic expansions give it a competitive edge. Despite a smaller market capitalization ($10B vs. $17B for Ball), Crown consistently delivers stronger returns than its larger competitor. The company's focus on cost discipline, innovation, and operational scale ensures it remains a highly profitable and resilient player in the global packaging industry.

Why is Crown interesting?

Higher Return on Assets: More capital-efficient than Ball, with consistently superior profitability.

Stronger Growth Profile: Expanding globally, benefiting from demand in soft drinks and emerging markets.

Attractive Valuation: Trades at a discount to Ball, with potential multiple expansion.

Valuation:

Crown trades at an EV/EBITDA multiple of 8.4x, significantly below Ball’s 11.0x 2025E multiple, making it a cheaper and lower-risk alternative. Given its higher returns, strong volume growth, and solid fundamentals, we see room for Crown’s multiple to move closer to Ball’s, unlocking upside potential for investors.

Enjoying the content? Don’t miss out on more exclusive insights and analyses. Upgrade to paid now and stay updated.

3. Post Holdings (POST):

Business Model:

Post Holdings operates as a diversified packaged food company, with strong brands across cereals, refrigerated foods, and foodservice. The company benefits from stable demand in its core segments while maintaining pricing power and operational efficiencies. Its Foodservice division plays a key role in profitability, with upside potential from improved margins, particularly if egg prices rise.

Beyond organic growth, capital allocation is a key driver of value creation. Post has historically pursued M&A as a long-term strategy, but in the absence of deals, management is expected to focus heavily on share buybacks. This flexibility, combined with a disciplined approach to cost management, positions Post for sustained earnings stability and incremental upside in a sector facing headwinds.

Why is Post interesting?

Resilient Earnings Profile: Consensus estimates appear solid, reducing downside risk.

Foodservice Upside: Margin expansion potential, particularly with higher egg prices.

Capital Allocation Focus: Strong likelihood of aggressive share buybacks in 2024.

Valuation:

Post trades at a 9.5x EV/EBITDA, which we see as offering more upside than downside risk given its earnings stability. While not as cheap as it once was relative to the food sector, the company maintains a disciplined capital allocation strategy, with potential for share repurchases to enhance shareholder value.

Now, let’s dive into the top 2…

Keep reading with a 7-day free trial

Subscribe to Jimmy's Journal to keep reading this post and get 7 days of free access to the full post archives.