Why Buffett Hates Airlines. A Case Study

A business built to fly, but not to compound: why airlines rarely deliver lasting shareholder value...

Hi, Investor 👋

I’m Jimmy, and welcome to another edition of our newsletter. In today’s issue, we’re unpacking why Warren Buffett steered clear of airline stocks - and what that tells us about tough industries, fragile economics, and the limits of scale.

Even essential businesses can destroy value if the structure is broken. Airlines are a case study in why moats matter more than market size.

Let’s jump in.

In case you missed it, here are some recent insights:

Subscribe now and never miss a single report:

“If a capitalist had been present at Kitty Hawk back in the early 1900s, he should have shot Orville Wright.” — Warren Buffett, 2007

For decades, Warren Buffett’s distaste for airline stocks has puzzled many investors.

How could a business so essential to global commerce, tourism, and modern life be so unattractive to one of the world’s most celebrated capital allocators?

To understand this paradox, we must go beyond the surface and examine the airline industry through the lens of strategic analysis, industry structure, and value creation.

The Economics of Value Creation:

At the core of any long-term investment thesis lies a simple equation:

Value creation = ROIC – WACC.

A company creates value only when its return on invested capital (ROIC) exceeds its weighted average cost of capital (WACC).

In industries where this spread is consistently negative, even operational improvements or revenue growth may fail to generate economic value.

The airline industry has a long and notorious history of earning ROICs at or below WACC.

In other words, despite growing revenues and essential services, the industry has historically destroyed shareholder value. From 1963 to 2023, U.S. airlines rarely posted positive ROIC-WACC spreads. This isn’t just a cyclical issue - it’s structural.

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

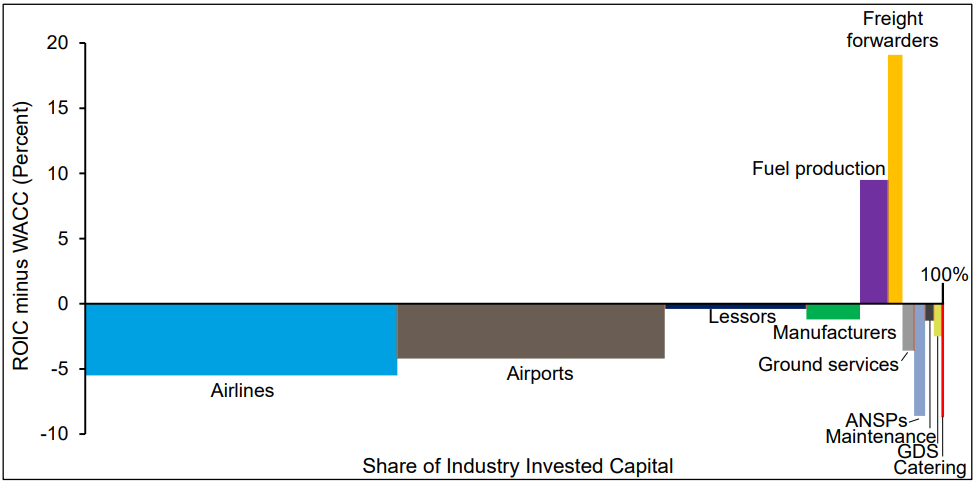

Understanding the Profit Pool:

In 2022, the aviation industry’s aggregate economic profit was negative $69 billion.

Most of the invested capital resides in asset-heavy segments like airlines and airports - both perennial underperformers.

By contrast, niche players such as freight forwarders and fuel suppliers generated modest positive economic profit despite their relatively small capital bases.

The implication is clear:

Even when the overall industry struggles, certain segments find ways to earn above their cost of capital. Airlines, however, seldom occupy those segments.

What Would Porter Say?

To further understand the competitive landscape, we turn to Michael Porter’s Five Forces framework.

The airline industry is, unfortunately, a textbook example of a structurally unattractive sector:

Rivalry Among Existing Competitors: Intense. Price wars are common. Differentiation is minimal. Customers view seats as commodities, and loyalty programs offer diminishing returns.

Threat of New Entrants: Moderate to high. While aircraft procurement and regulatory hurdles present barriers, the proliferation of low-cost carriers has shown that entry is possible - often with disruptive effects.

Bargaining Power of Suppliers: High. Aircraft and engine manufacturers (Airbus, Boeing, GE, Rolls-Royce) operate as oligopolies. Airports and labor unions also exert significant leverage.

Bargaining Power of Buyers: High. With near-zero switching costs, passengers chase the lowest fare. Online aggregators have further commoditized the booking process.

Threat of Substitutes: Medium. Alternatives like high-speed rail (Europe, China) or videoconferencing (post-COVID) are becoming more viable.

Each of these forces squeezes margins. Together, they form a gauntlet that makes sustainable value creation exceedingly rare.

Enjoying the content? Encourage me to keep creating more like this. Buy me a coffee!

The Illusion of Scale:

Airlines are enormous businesses with seemingly insurmountable capital requirements.

Yet, scale does not translate to moat…

The cost advantages of large fleets and extensive route networks are often offset by high fixed costs and cyclical demand.

Moreover, scale fails to inoculate carriers from exogenous shocks - oil prices, terrorism, weather events, pandemics. These “Black Swan” moments seem to hit airlines with greater frequency and ferocity than most sectors.

Despite post-COVID recovery, the U.S. airline industry as a whole still posted negative economic profit in 2023.

And here’s a revealing curiosity:

Most airlines must fill at least 70 - 80% of their seats just to break even.

That’s right!!!

The first two dozen passengers on your average domestic flight essentially cover fixed costs like fuel, crew, maintenance, and aircraft leasing. Only after the plane is mostly full do the economics start to work…

So the next time you find yourself in a half-empty cabin, ask yourself:

“How many flights like this can an airline survive?”

The answer explains a lot about Buffett’s skepticism…

Stability Without Strength:

Interestingly, the U.S. airline industry has become more stable in recent years.

Market share instability - a metric that gauges how much competition reshuffles share among incumbents - has fallen.

The “Big Four” carriers (Delta, United, American, and Southwest) control over 75% of the domestic market. Consolidation has improved pricing discipline and reduced irrational competition.

But stability ≠ profitability.

Even with higher concentration (Herfindahl-Hirschman Index rising), the underlying economics remain weak.

Without a mechanism to raise prices sustainably or reduce costs dramatically, stable market shares merely slow the bleeding.

Found this content valuable? Share it with your network! Help others discover these insights by sharing the newsletter. Your support makes all the difference!

The ROIC Trap:

Airlines face what we might call a “ROIC trap”:

Whenever one airline achieves a temporary cost or revenue advantage, competitors quickly replicate or undercut it.

This traps all players in a low-margin equilibrium. Worse, the high fixed-cost structure magnifies small miscalculations - making profitability fleeting and failure expensive.

It’s hard to build a durable moat when your product is a seat, your customer is disloyal, and your cost structure is rigid.

Network Effects ≠ Moat:

While some argue that airlines benefit from network effects, this is a misapplication of the concept.

True network effects - like those seen in software or marketplaces - become stronger as more users join.

Airline networks, by contrast, are expensive to maintain, hard to scale without incremental cost, and vulnerable to congestion and delays.

A United hub in Newark doesn’t necessarily benefit Delta in Atlanta. Route networks don’t confer winner-take-most economics.

Enjoying the content? Encourage me to keep creating more like this. Buy me a coffee!

Why Buffett Gave Up - And Then Dipped Back In:

Buffett’s distaste for airlines was long-held - and well-documented.

However, he famously changed his mind and bought stakes in Delta, United, American, and Southwest in the late 2010s, only to dump them in early 2020.

His rationale? Consolidation had improved discipline. ROIC was inching closer to WACC. Maybe, just maybe, the industry had turned a corner.

COVID proved otherwise.

The pandemic grounded fleets, collapsed demand, and forced government bailouts. Buffett exited completely.

His final assessment?

“The world changed.”

But perhaps it didn’t. Perhaps it merely revealed what was always true: airlines are structurally disadvantaged businesses, reliant on volume, vulnerable to shocks, and unable to build sustainable economic moats.

Strategic Takeaways:

The airline case study offers broader lessons:

Industry structure matters. Even great management teams can’t overcome poor structural economics.

Profit pools are uneven. Value tends to accrue to suppliers, intermediaries, and niche service providers - not always to the end producers.

Great businesses don’t fight the competition - they avoid it. Instead of battling for market share, they build moats that protect pricing and profitability.

Growth only creates value when ROIC exceeds WACC. Without a positive spread, scaling the business just scales the losses.

Buffett never bet against airplanes - he bet against the economics of the airline business.

And over the long run, he was right.

What’s your take on this? Share your thoughts in the comments.

Thanks for reading all the way through.

Until next time,

Jimmy

Disclaimer

As a reader of Jimmy’s Journal, you agree with our disclaimer. You can read the full disclaimer here.

Great metric to check.

If you wish to seek for a diamond screen for ROA > (4×Headline CPI Inflation Rate).

Assuming Core CPI USA 2025 3.2%:

4× Headline CPI Inflation Rate

= 4 × 3.2 %

= 12.8 %

ROA > 12.8 %